ACH Payments in Online Dating: Your 2026 Guide

ACH Payments in Online Dating: Your 2026 Guide

ACH payments in online dating are electronic bank-to-bank transfers that process recurring membership charges directly from your checking or savings account, bypassing card networks entirely. The Automated Clearing House (ACH) network is the standard industry term for this system, operated by Nacha, the governing body that sets the rules for all ACH transactions in the United States. About 80% of online dating payments still run through credit and debit cards, which means ACH is a specialized but powerful option for members who want lower fees and fewer billing interruptions. Platforms like Match Group properties and subscription-based dating services increasingly offer ACH as a secondary payment rail alongside cards, particularly for long-term members who want predictable, uninterrupted billing.

How do ACH payments work on online dating platforms?

ACH transfers in dating apps move money through the Nacha-operated network in a series of batched transactions rather than real-time authorizations. That process differs fundamentally from how a credit card works, and understanding the difference helps you set realistic expectations.

When you authorize an ACH payment on a dating platform, you provide your bank routing number and account number. The platform submits a debit request to the ACH network, which batches that request with others and sends it to your bank for processing. Settlement typically takes one to three business days, compared to the near-instant authorization you get with a Visa or Mastercard transaction.

For recurring billing, this timeline works well. Your monthly or annual subscription renews on a fixed schedule, so the platform initiates the debit days before your renewal date. The funds clear before your membership lapses. This is why ACH is best for recurring memberships rather than one-time or instant purchases where immediate payment confirmation matters.

Here is what the typical ACH subscription cycle looks like on a dating platform:

- Authorization: You provide bank account details and sign a written or electronic mandate authorizing recurring debits.

- Submission: The platform sends a debit entry to the ACH network on your scheduled billing date.

- Processing: The ACH network routes the request to your bank, which reviews available funds.

- Settlement: Funds transfer within one to three business days and the platform confirms your subscription renewal.

- Notification: You receive a billing confirmation by email, matching the descriptor on your bank statement.

Pro Tip: Save your ACH authorization confirmation email. If a billing dispute arises, that document proves you authorized the charge and speeds up resolution with both the platform and your bank.

The key distinction from card payments is the absence of instant validation. A credit card either approves or declines in seconds. An ACH debit can appear to succeed at submission but return as failed days later if your account has insufficient funds. Platforms account for this with retry logic built into their billing systems.

ACH vs. card payments for dating subscriptions: what’s the difference?

ACH and card payments each serve a distinct purpose in the online dating payment ecosystem. Choosing between them depends on your priorities: cost, speed, or billing continuity.

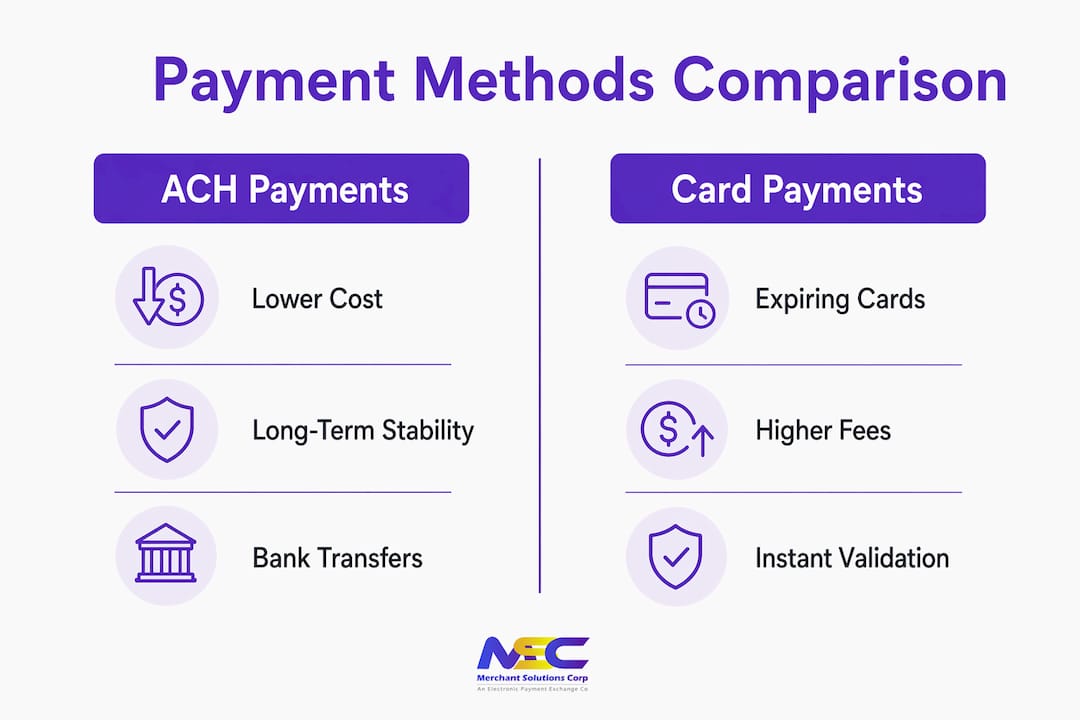

ACH transactions carry lower transaction costs than card network fees, which typically run in the range of 1.5–3.5% per transaction plus a fixed fee. ACH fees are generally a flat per-transaction amount, making them significantly cheaper for platforms processing high volumes of recurring subscriptions. Those savings can translate into lower subscription prices or more stable pricing over time.

Card payments, however, expire. When your credit card reaches its expiration date or gets replaced after fraud, your subscription stops unless you update your details. ACH payments tied to a bank account avoid this problem entirely. Your checking account number does not expire, which reduces the billing interruptions that cause members to unintentionally churn from dating platforms.

| Feature | ACH payments | Card payments |

|---|---|---|

| Transaction cost | Lower flat fee per transaction | Higher percentage-based fee |

| Settlement speed | 1–3 business days | Near-instant authorization |

| Expiration risk | None (bank accounts don’t expire) | High (cards expire every 2–4 years) |

| Instant purchase suitability | Poor | Excellent |

| Recurring billing stability | High | Moderate |

| Geographic availability | U.S. bank accounts only | Global |

| Chargeback risk | Moderate | Higher for dating platforms |

The table above shows that neither method wins across every category. ACH wins on cost and long-term billing stability. Cards win on speed and global reach.

ACH also has real limitations. It works only for U.S. bank accounts, which excludes international members entirely. It cannot support instant purchases like premium feature unlocks where the platform needs immediate payment confirmation before delivering access. Using ACH for instant purchases risks failed delivery because settlement has not yet cleared.

Pro Tip: If a dating platform offers both ACH and card payment options, consider using ACH for your base subscription and keeping a card on file for one-time premium purchases. That combination gives you the cost benefit of ACH without sacrificing instant access to features.

What security and compliance rules protect ACH payments in dating?

Security for ACH payments in dating platforms rests on two layers: Nacha’s operating rules and the platform’s own fraud controls. Both matter to you as a user.

Nacha operating rules require that every ACH debit carry a valid authorization from the account holder. That authorization must use specific language, be stored securely by the platform, and be retrievable if your bank requests proof during a dispute. Platforms that fail to meet these requirements risk account termination, which would disrupt service for all members. Compliance with Nacha rules is not optional. It is the foundation of every legitimate ACH transaction on a dating site.

Dating platforms carry the MCC 7273 merchant category code, which banks classify as high risk due to recurring billing disputes and elevated fraud rates. That classification means platforms must work with specialized payment processors who understand the compliance requirements specific to this industry. A mismatch between the payment gateway and the merchant account holder causes about 20% of payment setup failures on dating platforms. Choosing the wrong processor creates instability that affects every member’s billing.

From a user perspective, here is what legitimate ACH security looks like on a reputable dating platform:

- Encrypted data transmission: Your bank account details travel over encrypted connections and are stored using tokenization, meaning the platform never holds your raw account number after initial setup.

- Discreet billing descriptors: Reputable platforms use neutral or branded billing descriptors on your bank statement to protect your privacy.

- Fraud detection: Platforms use automated screening to flag unusual account activity before processing debits.

- Clear authorization language: When you set up ACH, the platform must show you explicit language stating the amount, frequency, and cancellation terms of the recurring debit.

- Return handling: If your bank returns a debit as unauthorized, the platform must follow Nacha’s rules on how many retry attempts are permitted and when to stop.

Payment gateways for dating sites also use 3DS 2.0 fraud screening for card transactions, and similar advanced fraud detection applies to ACH flows. That technology reduces friendly fraud, which is when a member authorizes a charge and then disputes it with their bank. If you ever receive an ACH debit you did not authorize, contact your bank immediately. Nacha rules give consumers the right to dispute unauthorized ACH debits within 60 days of the statement date.

How to set up and manage ACH payments on a dating platform

Setting up ACH on a dating platform takes a few minutes and requires only your bank’s routing number and your account number. Both appear on any personal check or in your bank’s mobile app.

- Navigate to payment settings. Log into your dating account and go to the billing or subscription section. Look for a bank account or ACH payment option alongside the standard card entry fields.

- Enter your bank details. Input your routing number (nine digits) and your checking or savings account number. Double-check both numbers before submitting. An error here causes a failed debit and a billing delay.

- Review the authorization agreement. The platform will display the recurring debit terms before you confirm. Read the amount, billing frequency, and cancellation policy. This document is your legal authorization under Nacha rules.

- Confirm and save. Submit your details. Some platforms use micro-deposit verification, sending two small test deposits to your account within one to two business days. You confirm the exact amounts to verify ownership before ACH billing activates.

- Set up renewal notifications. Enable email or app notifications for upcoming billing dates. ACH debits do not provide the instant confirmation that card charges do, so staying informed prevents surprises.

If an ACH payment fails, the platform’s billing system typically retries the debit after a short waiting period. Dunning and retry logic recover 15–30% of lost revenue from failed subscriptions on dating platforms. That means a single failed debit does not automatically cancel your membership. You will usually receive a notification asking you to verify your bank details or ensure sufficient funds before the next retry.

If retries continue to fail, update your payment method promptly to avoid a membership lapse. Some platforms allow you to temporarily switch to a card while resolving a bank account issue, then revert to ACH once the problem is fixed. ACH works best as a long-term, stable payment method for members who maintain consistent account balances and want uninterrupted access to premium features.

What future trends are shaping ACH payments in online dating?

Same-day ACH is the most significant near-term development for dating platform users. Nacha has expanded same-day ACH processing windows, which means platforms can now settle certain transactions within hours rather than days. That improvement reduces the gap between ACH and card payment speed, making ACH more practical for a broader range of transaction types on dating apps.

Integrating diverse payment methods including bank transfers can lift conversion rates, with some platforms reporting significant increases when they add locally preferred payment options. Digital wallets like PayPal and Venmo increasingly connect to ACH rails on the back end, giving users a familiar interface while the underlying transaction still moves through the bank network. That integration makes ACH more accessible to users who are comfortable with digital wallets but unfamiliar with direct bank entry.

Regulatory changes are also tightening compliance automation. Nacha continues to update its rules around return rate thresholds and authorization requirements, pushing platforms toward more sophisticated billing infrastructure. For users, that means better protections and clearer billing practices. For platforms, it means investing in specialized processors who stay current with Nacha rule updates.

International users remain excluded from ACH, which is a structural limitation. Cross-border payments on dating platforms still rely on card networks or alternative local payment methods. As dating platforms expand globally, they build multi-rail payment systems that route U.S. members through ACH while routing international members through cards or regional bank transfer networks. That architecture gives each user the most appropriate payment method for their location.

Key takeaways

ACH payments work best as a secondary billing method for U.S.-based dating platform members who want lower fees and uninterrupted recurring subscriptions, not as a replacement for card payments.

| Point | Details |

|---|---|

| ACH is for recurring billing | Use ACH for monthly or annual subscriptions, not instant feature purchases. |

| Lower cost than cards | ACH flat fees are cheaper than card network percentage fees for recurring charges. |

| No expiration risk | Bank accounts don’t expire, reducing involuntary membership cancellations. |

| Compliance protects you | Nacha rules require platforms to store your authorization and limit retry attempts. |

| U.S. only | ACH works only for U.S. bank accounts; international members need card alternatives. |

Why ACH deserves more credit than it gets in online dating

Most people who use dating platforms never think about how their subscription payment actually moves. They enter a card number, hit confirm, and move on. ACH sits in the background as the quieter, less glamorous option, and that reputation undersells what it actually does well.

The honest case for ACH in online dating comes down to one thing: loyalty. If you have been on a platform for a year or more, you are exactly the kind of member ACH was built for. Your subscription renews on a predictable schedule. You are not making impulse purchases. You want the billing to work without requiring your attention every month. ACH delivers that.

What most articles miss is the friction that card payments quietly create over time. Cards expire. Banks reissue them after fraud. You forget to update your payment details and your subscription lapses. You rejoin, sometimes at a higher price. ACH eliminates that entire cycle for U.S. members. The ACH payment stability benefit is real and measurable for anyone who has experienced an unwanted subscription interruption.

The compliance side matters more than most users realize. Platforms that cut corners on Nacha authorization requirements or work with processors not equipped for high-risk merchant accounts create instability that affects every member. When a platform loses its payment processing relationship, it disrupts service for everyone, not just the members who triggered the compliance issue. Choosing a platform that invests in proper ACH infrastructure is a form of consumer protection.

My practical advice: if your dating platform offers ACH and you plan to stay subscribed for six months or more, use it. Set up renewal notifications, keep your bank account funded on billing dates, and save your authorization confirmation. ACH is not exciting. It is reliable. For a recurring subscription, reliable beats exciting every time.

— Jonathan

How Merchantsolutionscorp supports dating platform payment processing

Dating platforms operate in one of the most demanding payment environments in the U.S. market. High chargeback rates, MCC 7273 classification, and Nacha compliance requirements demand a processor that understands the full picture.

Merchantsolutionscorp provides specialized payment processing built for high-risk merchant categories, including online dating. The platform supports ACH and card payment rails, retry and dunning logic for failed subscriptions, and discreet billing descriptors that protect member privacy. Compliance infrastructure meets current Nacha operating rules, reducing the risk of account termination that disrupts service for members. If your dating platform needs a payment solution that handles ACH, cards, and the compliance complexity of MCC 7273, Merchantsolutionscorp is built for exactly that environment.

FAQ

What is ACH payment in online dating?

ACH payment in online dating is a bank-to-bank electronic transfer that debits your checking or savings account directly to pay for a dating platform subscription. It bypasses card networks and typically settles within one to three business days.

Is ACH safer than a credit card for dating subscriptions?

ACH and credit cards both offer strong consumer protections, but they differ in how disputes work. Nacha rules give you 60 days to dispute an unauthorized ACH debit, while credit card chargeback windows vary by issuer. Both methods use encryption and fraud screening on reputable platforms.

Why did my ACH payment to a dating site fail?

ACH debits fail most often due to insufficient funds, an incorrect account number, or a bank block on ACH transactions. Most dating platforms retry the debit automatically. Update your bank details or ensure your account is funded before the next retry to avoid a membership lapse.

Can international users pay with ACH on dating platforms?

ACH is available only to holders of U.S. bank accounts. International members must use credit cards, debit cards, or locally supported payment methods. Dating platforms with global memberships typically offer card and regional bank transfer options for non-U.S. users.

How do I cancel an ACH authorization on a dating platform?

Cancel your ACH authorization through the platform’s billing settings before the next scheduled debit date. You can also notify your bank in writing to revoke the authorization, though contacting the platform directly is the faster and cleaner approach under Nacha guidelines.