ACH Processing for Gas Stations: 2026 Guide

ACH Processing for Gas Stations: 2026 Guide

![]()

ACH processing is defined as a batch-based electronic network that moves funds directly between bank accounts, and for gas station operators, it is one of the most cost-effective payment tools available. The formal industry term is Automated Clearing House (ACH) processing, governed by Nacha (formerly NACHA), the organization that sets the rules for all ACH participants in the United States. Two networks carry ACH traffic: FedACH, operated by the Federal Reserve, and The Clearing House’s RTP-adjacent ACH network. Understanding ACH processing explained for gas stations means knowing how these networks handle your fuel payments, fleet billing, and supplier transactions every business day. This guide covers the full transaction lifecycle, settlement timing, 2026 compliance updates, and practical steps to get more out of your ACH program.

How does ACH processing work for gas stations?

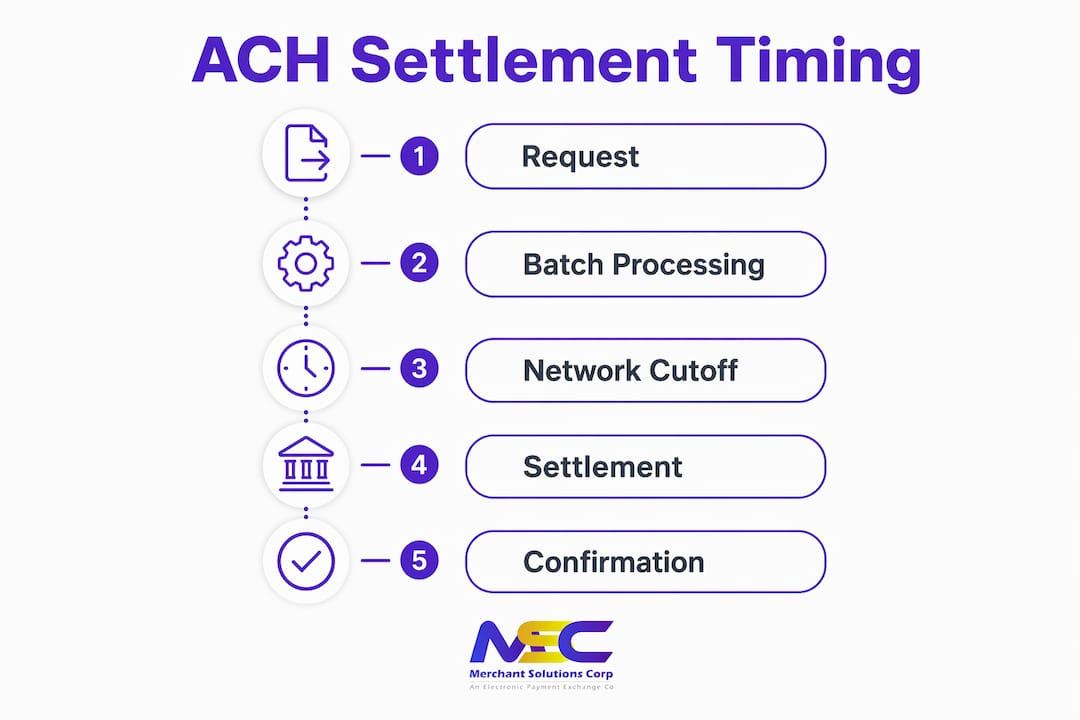

The ACH transaction lifecycle begins with the originator, which is either your gas station, your payment processor, or a third-party service provider acting on your behalf. That originator submits a payment instruction to the Originating Depository Financial Institution (ODFI), which is your bank or processor’s bank. The ODFI bundles those instructions into a Nacha-formatted batch file and sends it to one of the two ACH operators: FedACH or The Clearing House. The receiving bank, called the Receiving Depository Financial Institution (RDFI), then posts the debit or credit to the customer’s or vendor’s account.

This process is batch-based, not real-time. That distinction matters for gas station operators because it explains why funds do not appear instantly the way a card swipe might suggest. Payments move in scheduled waves throughout the business day, which creates predictable settlement windows you can plan around.

Gas stations use two types of ACH entries. ACH debits pull funds from a customer’s or fleet account into your account, which is the most common structure for recurring fuel billing. ACH credits push funds outward, typically used when you pay a fuel supplier or reimburse a vendor. Knowing which entry type applies to each transaction helps you set up your payment workflows correctly from the start.

Here is the step-by-step lifecycle specific to a gas station ACH debit:

- Authorization collected. Your customer or fleet account holder signs an ACH authorization form granting permission to debit their bank account.

- Originator submits the entry. Your payment processor or your station’s accounting system creates the ACH entry and sends it to the ODFI.

- ODFI batches and transmits. The ODFI compiles entries into a Nacha-formatted file and forwards it to FedACH or The Clearing House.

- ACH operator routes the file. The operator sorts entries by routing number and delivers them to the appropriate RDFIs.

- RDFI posts the transaction. The receiving bank debits the customer’s account and sends settlement funds back through the network.

- Settlement completes. Funds land in your account, typically within one to two business days for standard ACH.

Pro Tip: Set up your ACH entries through a payment processor that provides real-time status updates. Knowing whether a transaction is initiated, in transit, or settled prevents you from spending funds that have not yet cleared.

What are the timing and cutoff windows for ACH settlements?

Standard ACH transactions settle in one to three business days, which is the baseline most gas station operators work with. That timeline means a Monday morning debit typically posts to your account by Tuesday or Wednesday. Weekends and federal holidays do not count as business days, so a Friday submission may not settle until the following Tuesday if Monday is a holiday.

Same Day ACH changes this equation significantly. Nacha introduced Same Day ACH to allow faster settlement for eligible transactions, and it operates on three daily cutoff windows:

- 10:30 a.m. ET: Entries submitted before this window settle the same afternoon.

- 2:45 p.m. ET: The second window for same-day settlement.

- 4:45 p.m. ET: The final window, with settlement typically by end of business.

These are network-level deadlines. Your actual internal cutoff must be earlier. Same Day ACH requires operational discipline around internal submission times set well ahead of network deadlines to avoid fallback to standard ACH. If your processor’s internal cutoff is 9:30 a.m. ET for the first window, submitting at 10:15 a.m. means your entry misses same-day settlement entirely.

For gas station operators managing fleet accounts or high-volume fuel billing, Same Day ACH is a practical tool for improving cash flow. A fleet customer’s weekly fuel invoice can settle the same day it is sent rather than sitting in transit for two business days. That difference compounds quickly when you are processing dozens of fleet accounts each week.

A few additional timing factors deserve attention:

- Returns: A returned ACH entry, such as an insufficient funds return, adds one to two business days to your resolution timeline.

- Holidays: Nacha publishes an annual holiday schedule. Entries submitted the day before a holiday follow the next available processing window.

- Processor posting schedules: Some processors post settlements once daily. Others post multiple times. Confirm your processor’s schedule so your reconciliation reflects actual posting times, not assumed ones.

Stat to know: Same Day ACH cutoff windows at 10:30 a.m., 2:45 p.m., and 4:45 p.m. ET give gas stations up to three opportunities per business day to accelerate settlement. That flexibility is only useful if your internal workflow is built to meet those windows consistently.

How do nacha rules and 2026 updates affect fuel retailers?

Nacha governs every participant in the ACH network, including gas stations that originate ACH debits for fleet billing or recurring fuel payments. Compliance is not optional. Violating Nacha rules exposes your station to fines, increased return rate thresholds, and potential suspension from the ACH network.

The most significant change for 2026 is Nacha’s expanded fraud monitoring requirement. Nacha’s 2026 rule updates require all non-consumer originators, which includes gas stations, to implement and annually review risk-based fraud detection and monitoring processes tailored to their transaction volume and risk profile. This is not a one-time setup. You must document your monitoring approach, review it every year, and adjust it as your transaction patterns change.

Practical compliance steps for gas station operators include:

- Account verification before first debit. Use a bank account verification service to confirm routing and account numbers before initiating any ACH entry. This reduces return rates and fraud exposure.

- Transaction velocity monitoring. Flag unusual spikes in transaction volume or dollar amounts. A fleet account that normally runs $2,000 per week should trigger a review if it suddenly hits $15,000.

- Authorization documentation. Every ACH debit requires a signed authorization. ACH authorization forms must include payment amounts, timing, revocation rights, and procedures for handling bank account changes. Retain these records for at least two years.

- Return rate tracking. Nacha sets return rate thresholds for different return codes. Exceeding those thresholds signals a compliance problem. Monitor your return rates monthly.

- Dispute management process. Have a documented process for handling unauthorized transaction claims. Respond within the required timeframe to avoid escalation.

Pro Tip: When a fleet customer changes banks, collect a new signed authorization form before initiating the next debit. Debiting a closed or changed account generates a return and a potential unauthorized transaction claim, both of which damage your compliance standing.

The 2026 updates also extend some fraud monitoring obligations to third-party senders, meaning if you use a payment processor or fleet billing platform to originate ACH entries on your behalf, you share responsibility for ensuring that platform meets Nacha’s fraud monitoring standards. Ask your processor directly how they document and review their fraud controls.

What best practices optimize ACH acceptance and reconciliation?

Integrating ACH payment statuses into your POS and accounting systems is the single most effective step for improving financial visibility at your gas station. Without that integration, you are manually matching bank deposits to invoices, which creates errors and delays. With it, your accounting software knows whether a payment is initiated, in transit, settled, or returned before you ever open a bank statement.

Reconcile by settlement date, not by the date you initiated the transaction. This is a common source of cash flow confusion for gas station operators. An ACH debit initiated on Monday does not represent available funds until it settles, typically Wednesday. Booking it as received on Monday overstates your cash position and creates reconciliation gaps at month end.

The table below compares standard ACH and Same Day ACH across the dimensions that matter most for gas station financial operations:

| Factor | Standard ACH | Same Day ACH |

|---|---|---|

| Settlement timeline | 1–3 business days | Same business day |

| Cutoff windows | Varies by processor | 10:30 a.m., 2:45 p.m., 4:45 p.m. ET |

| Best use case | Recurring fleet billing | Urgent supplier payments |

| Return handling | 1–2 additional days | Same timeline as standard |

| Cost | Lower per-transaction | Slightly higher per-transaction |

| Cash flow impact | Moderate delay | Faster availability |

For gas stations managing fleet accounts, recurring payment structures are the most efficient ACH application. Set up a fixed billing cycle, collect signed authorizations upfront, and automate the debit schedule through your payment processor. This reduces manual entry, lowers the risk of missed payments, and gives fleet customers a predictable billing experience.

When bank account details change, update your authorization records immediately. Maintaining controls for ACH debit returns requires clear, regularly updated authorization forms that capture payment terms and account-change procedures. A single outdated routing number generates a return, a delay, and a compliance flag.

Technology selection matters here. Look for a payment processor that offers ACH status tracking, automated return notifications, and direct integration with accounting platforms like QuickBooks or your fuel management software. The EMV and ACH payment infrastructure at your pump and inside your store should feed into a single reconciliation workflow, not two separate systems you have to manually reconcile at the end of each day.

Pro Tip: Build your internal ACH submission schedule around your processor’s cutoff times, not the Nacha network deadlines. If your processor batches at 9:00 a.m. for the first Same Day ACH window, your entries need to be ready by 8:45 a.m. at the latest.

Key takeaways

ACH processing for gas stations works best when it is treated as a controlled payment process with clear authorization records, settlement-based reconciliation, and fraud monitoring that meets Nacha’s 2026 standards.

| Point | Details |

|---|---|

| ACH is batch-based, not real-time | Settlement takes 1–3 business days for standard ACH; plan cash flow accordingly. |

| Same Day ACH has three cutoff windows | Submit before 10:30 a.m., 2:45 p.m., or 4:45 p.m. ET to settle the same business day. |

| 2026 Nacha rules require fraud monitoring | Non-consumer originators like gas stations must implement and annually review risk-based fraud controls. |

| Reconcile by settlement date | Booking ACH entries on initiation date overstates cash position and creates accounting errors. |

| Authorization forms must be current | Update signed ACH authorizations whenever a customer’s bank account changes to avoid returns and compliance issues. |

ACH payments at gas stations: what i’ve learned watching operators get it wrong

Most gas station operators who struggle with ACH are not making errors on the technical side. They are treating ACH like a passive system where you set it up and collect money. That mindset creates real problems.

The operators who run clean ACH programs treat every debit like a controlled transaction. They know their return rates. They review their authorization files quarterly. They have someone accountable for reconciliation by settlement date, not by the date the entry was submitted. That discipline is what separates a smooth ACH program from one that generates disputes, return fees, and compliance headaches.

The 2026 Nacha fraud monitoring requirement is not a burden. It is a forcing function that pushes gas station operators to build the kind of oversight they should have had all along. Velocity monitoring and account verification are not just compliance checkboxes. They protect your revenue from fraudulent fleet accounts and unauthorized debits.

One area I see consistently underestimated is the gap between when an ACH entry is initiated and when it actually settles. Operators pull a report showing $40,000 in ACH debits submitted Monday morning and assume that money is available. It is not. Building your cash flow model around settlement dates rather than initiation dates is a small change that prevents significant confusion.

The stations that get the most value from ACH are the ones that connect it directly to their gas station payment solutions and accounting workflows. When your POS system, your ACH processor, and your accounting software all speak the same language, reconciliation becomes a daily routine rather than a monthly fire drill.

— Jonathan

How Merchantsolutionscorp supports gas station ACH processing

Merchantsolutionscorp works with gas station operators across the US to set up ACH payment acceptance that connects directly to your POS system and accounting workflow. The platform handles both credit card and ACH payment processing, with setup designed for fuel retail environments where speed, accuracy, and compliance all matter. Merchantsolutionscorp also offers dual pricing options that help offset processing costs, so ACH becomes an even more attractive payment channel for your fleet customers. If you are ready to build a payment system that handles ACH, card, and cash under one roof, explore the full range of payment processing solutions available for gas station operators today.

FAQ

What is ACH processing for gas stations?

ACH processing is a batch-based electronic payment method that moves funds between bank accounts through the Nacha-governed network, used by gas stations to collect fleet payments, pay suppliers, and manage recurring billing.

How long does an ACH payment take to settle?

Standard ACH settles in one to three business days. Same Day ACH reduces this to hours if your entry is submitted before the 10:30 a.m., 2:45 p.m., or 4:45 p.m. ET cutoff windows.

What nacha compliance rules apply to gas stations in 2026?

Gas stations that originate ACH debits must implement risk-based fraud monitoring and review it annually under Nacha’s 2026 rule updates. This includes velocity monitoring, account verification, and documented authorization management.

What should an ACH authorization form include?

A valid ACH authorization form must include the payment amount, billing frequency, revocation rights, and a procedure for handling bank account changes. Retain completed forms for at least two years to meet Nacha documentation standards.

How do gas stations reconcile ACH payments accurately?

Reconcile ACH entries by their settlement date, not the initiation date, to reflect actual cash availability. Integrating ACH status tracking with your POS and accounting software eliminates manual matching and reduces end-of-month errors.