Merchant Onboarding Workflow: A Small Business Guide

Merchant Onboarding Workflow: A Small Business Guide

A merchant onboarding workflow is a coordinated series of steps designed to verify business identity, assess risk, and enable secure payment acceptance quickly and reliably. For small business owners, this process is the difference between accepting your first transaction within 24 hours or waiting days while paperwork stalls in a manual review queue. The industry term for this end-to-end process is “merchant activation,” and it covers everything from initial data collection through Know Your Business (KYB) compliance checks to payout account validation. When your merchant onboarding process is structured correctly, you reduce failed payouts, avoid compliance gaps, and build the kind of trust with payment processors that keeps your account in good standing long-term.

What are the essential steps in a merchant onboarding workflow?

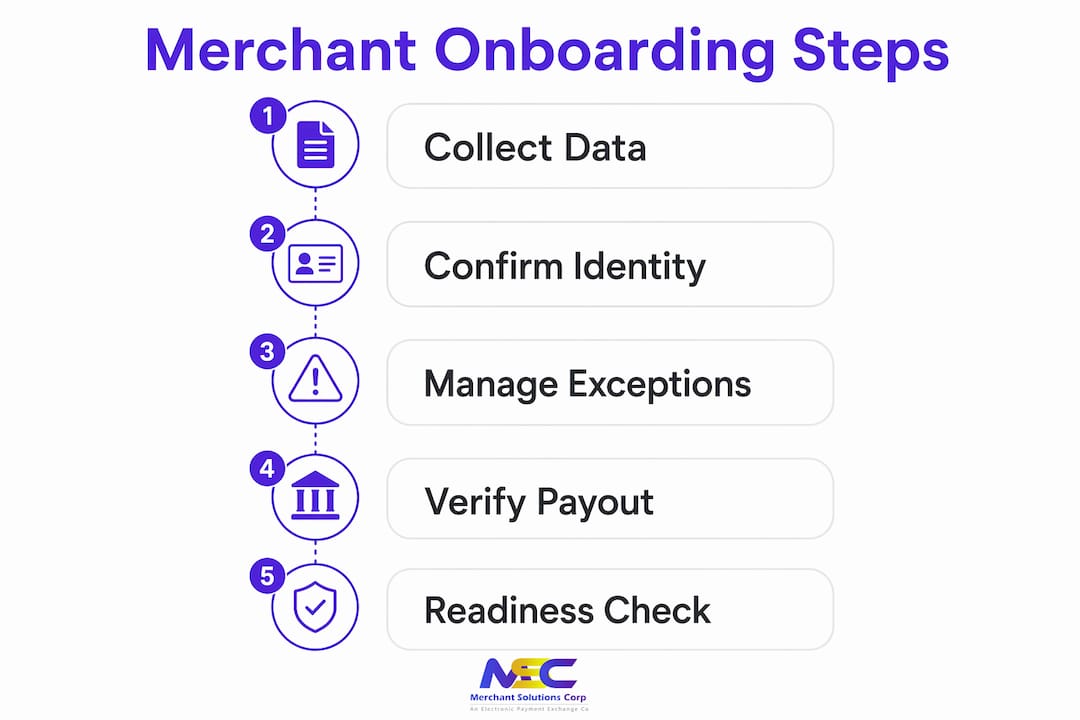

A well-designed merchant onboarding workflow follows five structured stages: gather merchant data, confirm identity, handle exceptions, verify payout accounts, and confirm first-payout readiness. Each stage serves a distinct purpose, and skipping or combining them is the most common reason onboarding fails.

Step 1: Collect merchant information and determine the onboarding path

The first step is gathering the business details that define every subsequent decision. This includes legal business name, tax identification number (EIN or SSN for sole proprietors), business type, industry category, and estimated transaction volume. The data you collect here determines whether the merchant follows a standard approval path or gets routed to a more intensive review.

Getting this step right matters more than most business owners realize. Incomplete or inconsistent data at intake creates cascading problems. A restaurant that lists its business name differently on its bank account versus its application will trigger a mismatch flag later in payout verification.

Step 2: Confirm identity and perform KYB and KYC checks

Know Your Business (KYB) verification confirms that the business legally exists and that the people controlling it are who they claim to be. KYB verification includes verifying company existence, confirming directors, and identifying ultimate beneficial owners (UBOs), which are individuals who own 25% or more of the business. Know Your Customer (KYC) checks run parallel, verifying the identity of the primary account holder through government-issued ID and sometimes biometric confirmation.

This step applies to every merchant, including small and new businesses. Skipping UBO identification because a business seems low-risk is a compliance gap that regulators and payment networks treat seriously.

Step 3: Manage exceptions and high-risk case reviews

Not every application clears automated checks. Exception handling requires clear review criteria and defined workflows to prevent bottlenecks when onboarding high-risk or incomplete applications. A merchant flagged for an unusual ownership structure, a restricted industry category, or a mismatched document needs a defined escalation path, not a generic hold.

Pro Tip: Build a tiered exception queue with defined turnaround times. A 24-hour SLA for standard exceptions and a 72-hour SLA for complex cases prevents applications from aging indefinitely and reduces merchant frustration.

Step 4: Collect and verify payout account details

Payout account verification confirms that the bank account where funds will be deposited belongs to the merchant and is capable of receiving ACH transfers. This step is separate from identity verification and should be treated as its own control. Identity and payout verification serve distinct roles; conflating them leads to operational issues and risk gaps.

Tools like Plaid’s bank account linking API can verify account ownership instantly by connecting directly to the merchant’s bank, eliminating the multi-day wait for micro-deposit confirmation.

Step 5: Perform first-payout readiness checks

Before the first payout is released, a final readiness check confirms that all controls are in place. This includes confirming that KYB and KYC checks are complete, that the payout account is verified and matches the business identity, and that transaction monitoring rules are active. Structuring onboarding checkpoints into identity verified, payout account verified, and first-payout readiness enables smoother technical integration and reduces failures.

| Step | Purpose |

|---|---|

| Collect merchant data | Establishes the onboarding path and flags potential risk factors early |

| KYB and KYC verification | Confirms legal business existence and owner identity |

| Exception handling | Routes flagged applications to the correct review tier |

| Payout account verification | Confirms bank account ownership and ACH eligibility |

| First-payout readiness | Final check that all controls are active before funds move |

How can automation and digital tools speed up the merchant onboarding process?

Automation is the single biggest lever for reducing onboarding time without increasing compliance risk. Automated KYB reduces onboarding times from several days to under 24 hours by integrating verification APIs, document OCR, and risk scoring for auto-approval. That shift from days to hours directly affects how quickly a merchant can start accepting payments and generating revenue.

The key is knowing which parts of the workflow to automate first. Not all steps carry equal risk, and not all automation tools are equal in quality.

Here are the areas where automation delivers the clearest return:

- Identity and business verification APIs. Services that connect directly to government business registries and credit bureaus confirm business existence and director information in seconds, replacing manual document review for standard cases.

- Bank account linking. Tools that use open banking connections verify payout account ownership instantly, removing the 2 to 3 day wait for micro-deposit confirmation.

- Document OCR and data extraction. Optical character recognition pulls data from uploaded IDs and business documents directly into your onboarding system, eliminating manual re-entry and the errors that come with it.

- Dynamic risk-based routing. Automated risk scoring assigns each application a risk tier at intake, routing low-risk merchants to instant approval and flagging higher-risk cases for human review. This keeps your review team focused on cases that actually need attention.

- E-signature and consent capture. Combining document capture, e-sign consent, and instant payment provisioning improves user experience and auditability in a single workflow step.

Pro Tip: When building your automation stack, prioritize data field validation at the point of entry rather than at the end of the workflow. Catching a missing EIN or a misformatted routing number at intake costs seconds. Catching it after a KYB check has already run costs hours and sometimes requires restarting the entire verification process.

Platforms like Ultra Commerce offer retail and marketplace infrastructure that integrates verification and payment activation into a single coordinated flow, which is particularly useful for businesses onboarding multiple merchant locations or product vendors at scale.

The practical result of well-designed automation is measurable. Merchants who experience a fast, clear onboarding process are significantly more likely to complete activation and start transacting. Every additional step that requires manual input or a wait period is a point where merchants abandon the process entirely.

How to handle risks and approvals during merchant onboarding

Risk management in merchant onboarding is not about blocking merchants. It is about making accurate, fast decisions that protect your business and your payment processor from fraud, chargebacks, and regulatory penalties.

KYB risk assessment covers four primary areas:

- Business existence and legal standing. Is the business registered with the appropriate state or federal authority? Is it in good standing, or has it been dissolved or flagged?

- Director and UBO identification. Who controls the business? KYB verification must include director and ultimate beneficial owner identification even for small or new merchants to enable trustworthy onboarding decisions.

- Industry and geography risk. Certain industries carry higher chargeback rates or regulatory scrutiny. Businesses in categories like firearms, nutraceuticals, or adult content require additional review. Geography matters too, particularly for businesses with international ownership structures.

- Transaction volume and ownership complexity. A sole proprietor processing under $10,000 per month carries a different risk profile than a multi-location LLC with three beneficial owners and projected six-figure monthly volume.

Risk scoring models assign a numerical score based on these factors and route each application accordingly. A tiered review workflow might look like this:

- Score 0 to 40 (low risk): Auto-approve with standard monitoring

- Score 41 to 70 (medium risk): Approve with enhanced transaction monitoring and a 90-day review

- Score 71 and above (high risk): Route to manual review with a defined SLA

For businesses that fall into the high-risk merchant category, the onboarding path is longer but not impossible. Specialized processors and platforms like Merchantsolutionscorp have industry-specific setups designed for these cases.

Ongoing monitoring with transaction-monitoring rules and automated sanctions re-screening updates risk profiles over time, detecting changes after onboarding. A merchant who was low-risk at activation can become higher-risk if their transaction patterns shift significantly or if a director is added who appears on a sanctions list.

One recent regulatory development worth noting: FinCEN exceptive relief allows beneficial ownership verification to be collected initially and updated only when reasonable risk triggers occur, reducing repetitive data requests. This eases the administrative burden on small businesses without weakening compliance controls.

What are common pitfalls in merchant onboarding workflows and how to avoid them?

Most onboarding failures trace back to a small number of recurring problems. Identifying them in advance is far less costly than fixing them after a payout fails or a compliance audit surfaces a gap.

Manual data entry errors. When merchants type their business name, EIN, or bank routing number into a form, errors are inevitable. A single transposed digit in a routing number causes a payout to fail. The fix is inline validation at the point of entry, not a batch check at the end of the process.

Inconsistent ownership and payout account data. Onboarding delays often stem more from inconsistent ownership and payout account data than from wait times for approvals. A business registered under “Smith Retail LLC” that submits a bank account in the name of “John Smith” will trigger a mismatch that requires manual resolution. Treating KYB and payout account verification as tightly coupled workflows, where the business identity confirmed in step two must match the account holder confirmed in step four, prevents this problem entirely.

Poor communication and unclear expectations. Merchants who do not know what documents they need, how long the process takes, or what happens if their application is flagged will abandon the process. A simple onboarding checklist sent at the start, combined with automated status updates at each stage, reduces abandonment significantly.

“A digitally coordinated onboarding workflow that combines document capture, e-sign consent, and instant payment provisioning improves user experience and auditability.” — docscan.cloud

Inadequate audit trails. Audit trail completeness in digital onboarding, including timestamps, device metadata, consent versioning, and document hashes, is critical for compliance and dispute resolution. If a merchant later disputes a charge or a regulator requests proof of consent, an incomplete audit trail creates serious liability. Every onboarding system should capture the IP address, device type, timestamp, and consent version for every signature and document submission.

Pro Tip: Structure your onboarding into three explicit checkpoints: identity and KYB verified, payout account verified, and first-payout readiness confirmed. Treat each checkpoint as a gate. A merchant cannot advance to the next stage until the previous one is complete. This prevents partial onboarding, where a merchant appears active in your system but is missing a critical control.

Key takeaways

A merchant onboarding workflow succeeds when identity verification, payout account validation, and risk controls operate as distinct, sequential checkpoints rather than overlapping or skipped steps.

| Point | Details |

|---|---|

| Five-step structure | Follow the collect, verify, handle exceptions, validate payout, and confirm readiness sequence to reduce errors. |

| KYB and KYC are non-negotiable | Verify business existence, directors, and UBOs for every merchant, including small and new businesses. |

| Automate at the right points | Use verification APIs and bank linking tools to cut approval times from days to under 24 hours. |

| Audit trails prevent disputes | Capture timestamps, device metadata, and consent versions at every onboarding stage for compliance protection. |

| Ongoing monitoring matters | Post-approval transaction monitoring and sanctions re-screening catch risk changes that occur after activation. |

Why most onboarding problems are actually data problems

After working through merchant activation processes across restaurants, retail, and service businesses, one pattern stands out clearly. The businesses that struggle most with onboarding are not the ones with complex ownership structures or unusual industries. They are the ones that treat data collection as an afterthought.

The instinct is to get merchants activated as fast as possible, which often means rushing through the intake form and fixing problems later. That approach costs more time than it saves. A mismatched business name between the KYB record and the payout account does not get resolved in five minutes. It requires a manual review, sometimes a document request, and occasionally a full re-verification.

The smarter approach is to invest in the front end of the workflow. Build validation logic into every data field. Confirm that the business name on the application matches the bank account name before the merchant reaches step four. Use open banking connections to verify account ownership at the moment of submission rather than days later.

Merchantsolutionscorp has seen this play out consistently with small business clients. The ones who complete onboarding fastest are the ones who come prepared with clean, consistent documentation. When the workflow is designed to guide merchants toward that preparation rather than simply collecting whatever they submit, activation rates improve and support tickets drop.

The other insight worth sharing is that compliance and speed are not opposites. A well-designed workflow with automated KYB, instant bank account linking, and dynamic risk routing can approve a standard merchant in under 24 hours while maintaining every required control. The businesses that treat compliance as a slowdown are usually working with a poorly designed process, not an inherently slow one.

— Jonathan

How Merchantsolutionscorp simplifies your merchant onboarding workflow

Merchantsolutionscorp is built for small businesses that need to start accepting payments without weeks of back-and-forth. The platform covers credit card and ACH processing with fully configured POS systems including Clover and mobile terminals, and the onboarding process is designed to get you operational fast. Applications are reviewed with industry-specific risk assessments, so whether you run a retail shop, a restaurant, or a service business, your setup reflects your actual needs. Merchantsolutionscorp also supports retail payment solutions with $0 upfront hardware options and dual pricing to offset processing fees. If you are ready to move from application to first transaction without the friction, Merchantsolutionscorp has the process and the support to make it happen.

FAQ

What is a merchant onboarding workflow?

A merchant onboarding workflow is the structured process a payment processor or platform uses to verify a business’s identity, assess risk, and activate payment acceptance. It typically includes KYB and KYC verification, payout account validation, and first-payout readiness checks.

How long does merchant onboarding take?

Standard merchant onboarding takes anywhere from a few hours to several days depending on the complexity of the application. Automated KYB systems can reduce approval times to under 24 hours for low-risk merchants.

What is KYB and why does it matter for small businesses?

KYB stands for Know Your Business, and it is the process of verifying that a business legally exists and that its owners are who they claim to be. KYB applies to all merchants, including small and new businesses, because payment processors are required to confirm business identity before enabling payment acceptance.

What causes merchant onboarding delays?

Onboarding delays most often result from inconsistent data between the business identity record and the payout bank account, missing documentation, or applications flagged for manual review due to risk scoring. Inline data validation and automated bank account linking address the majority of these delays.

What is an audit trail in merchant onboarding?

An audit trail is a complete record of every action taken during the onboarding process, including timestamps, device metadata, consent versions, and document submissions. A complete audit trail is required for regulatory compliance and is critical for resolving disputes if a merchant later challenges a charge or agreement.

Recommended

- Set up payment processing: a simple guide for small businesses | Merchant Solutions Corp

- Accept online payments: low-cost solutions for SMBs | Merchant Solutions Corp

- How to Implement a Compliant Cash Discount Program | Merchant Solutions Corp

- Payment Processing for Accountants | ACH, Recurring & POS | MSC