Motel Credit Card Processing: Industry Standards Guide

Motel Credit Card Processing: Industry Standards Guide

Industry standards for motel credit card processing are defined by PCI DSS compliance mandates, card network rules, and 2026 financial regulations that collectively establish rigorous security and operational protocols for every property accepting card payments. The Payment Card Industry Data Security Standard (PCI DSS) is the recognized industry framework governing how motels collect, transmit, and store cardholder data. Most independent motels fall under merchant Level 3 or Level 4, which determines the scope of your annual self-assessment and the cost of staying compliant. Getting this right protects your guests, reduces your chargeback exposure, and keeps your payment processor relationship intact.

What are the PCI DSS compliance levels and requirements for motels?

PCI DSS classifies merchants into four levels based on annual transaction volume, and most independent motels qualify as Level 3 or Level 4. Level 4 covers merchants processing fewer than 20,000 Visa e-commerce transactions annually or up to one million total transactions. Level 3 applies to merchants processing between 20,000 and one million Visa e-commerce transactions per year. Your level determines which Self-Assessment Questionnaire (SAQ) you must complete and how frequently you need to run vulnerability scans.

Understanding SAQ types for motels

The SAQ type you complete depends entirely on how your property handles cardholder data. Here is a breakdown of the four most relevant SAQ types for motel operators:

-

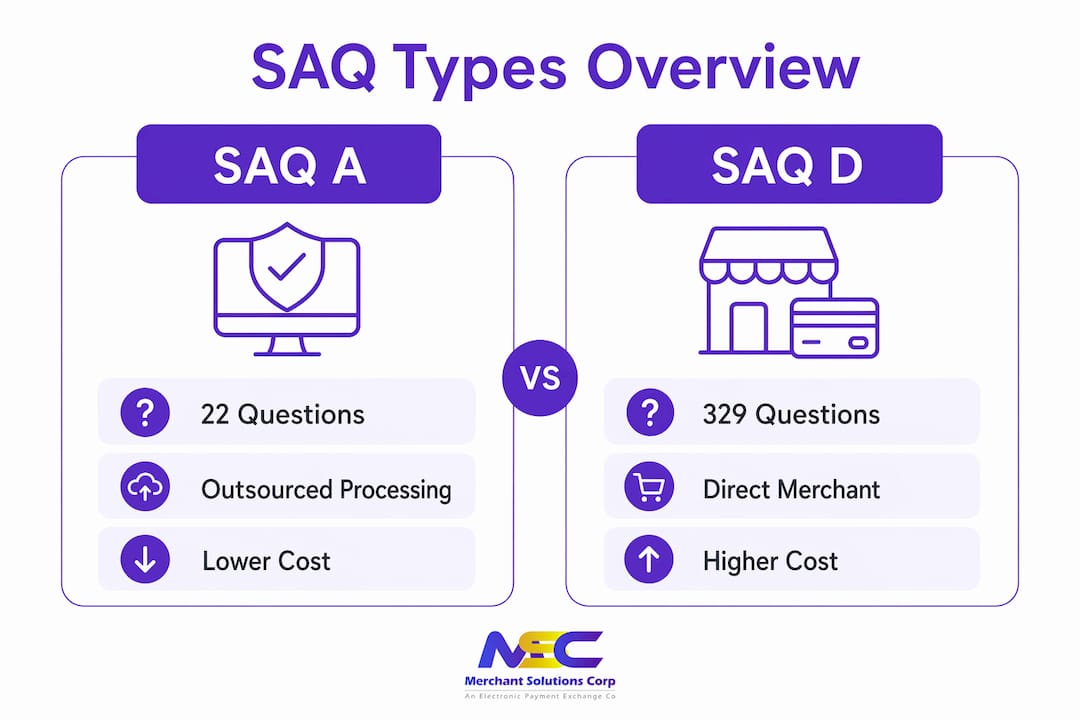

SAQ A covers motels that fully outsource all card processing to a PCI DSS compliant third party and never touch cardholder data directly. This is the lightest compliance path, requiring only 22 questions. It is the target configuration for most independent motels.

-

SAQ A-EP applies when your booking website redirects to a third-party payment page but your server still delivers that page. The presence of JavaScript elements like analytics or chat widgets on your booking page can pull you into this category under PCI DSS v4.0.1.

-

SAQ B-IP covers motels using IP-connected payment terminals that do not store card data. This is common for front desk terminals connected to a cloud-based property management system (PMS).

-

SAQ D is the most demanding category. It applies when your PMS or local server stores, processes, or transmits cardholder data. SAQ D contains approximately 300 questions and carries annual compliance costs ranging from $4,000 to $20,000.

The financial difference between SAQ types is significant. Switching from SAQ D to SAQ A reduces your compliance question count from roughly 300 to just 22, cutting audit time and cost dramatically. The trade-off is that you must completely outsource card data storage to a validated third party, removing your PMS from scope entirely.

| SAQ Type | Questions | Best For | Estimated Annual Cost |

|---|---|---|---|

| SAQ A | 22 | Fully outsourced card processing | Low ($500–$2,000) |

| SAQ A-EP | ~190 | Third-party page, motel-hosted scripts | Moderate ($2,000–$6,000) |

| SAQ B-IP | ~130 | IP-connected terminals, no stored data | Moderate ($1,500–$5,000) |

| SAQ D | ~300 | Local card data storage in PMS | High ($4,000–$20,000) |

Quarterly external vulnerability scans are required for most SAQ types. These scans must be conducted by an Approved Scanning Vendor (ASV) recognized by the PCI Security Standards Council. Annual self-assessments and scans together form the baseline compliance cycle for motel operators.

Pro Tip: If your current PMS stores card numbers locally, ask your vendor whether a tokenized integration is available. Moving to a tokenized setup can shift you from SAQ D to SAQ A and eliminate the bulk of your annual compliance burden.

What 2026 payment processing regulatory updates affect motels?

Two major regulatory changes took effect in 2026 that directly affect how motels process credit and debit card transactions. Understanding both is non-negotiable for staying compliant and avoiding financial penalties.

Regulation II dual-routing expansion

Starting July 1, 2026, US merchants must offer at least two unaffiliated debit card networks for online transactions. This expands the Regulation II dual-routing requirement, which previously applied only to card-present transactions at physical terminals. For motels accepting debit cards through online booking platforms or front desk software, this means your payment processor must support routing through a second, unaffiliated network such as NYCE, Pulse, or Star alongside Visa or Mastercard’s debit networks.

The practical implication is real. If your current payment gateway or processor does not support dual-routing for card-not-present debit transactions, you are out of compliance as of July 1, 2026. Contact your acquirer or processor now to confirm their routing capabilities and request written confirmation of compliance.

Interchange fee restrictions on taxes and gratuities

US interchange fee regulations now prohibit fees on tax and gratuity amounts, effective July 1, 2026. Violations carry a penalty of $1,000 per transaction. This means your payment system must correctly separate and transmit tax and gratuity amounts in transaction data so that interchange fees are not calculated on those portions. For motels that charge resort fees, parking fees, or incidental deposits, accurate line-item transmission is now a compliance requirement, not just a billing preference.

Additional 2026 security mandates affecting motels include:

- Multifactor authentication (MFA): PCI DSS v4.0.1 requires MFA for all administrative access to cardholder data environments, including your PMS login and payment gateway dashboard.

- Script integrity checks: PCI DSS v4.0.1 mandates script integrity controls on payment pages that embed third-party scripts. If your booking page loads Google Analytics, a live chat widget, or a review platform script, each must be inventoried and integrity-verified.

- Incident response plans: Processors and acquirers now require documented incident response procedures from lodging merchants as a condition of maintaining merchant accounts.

Motels that proactively audit their payment stack against these requirements before a processor review will avoid the account holds and fines that catch unprepared operators off guard.

What lodging-specific payment standards should motel owners follow?

Motels operate under a distinct set of payment processing norms that differ from retail or restaurant environments. Pre-authorization workflows, chargeback management, and merchant category code (MCC) selection each carry compliance and revenue implications specific to the lodging sector.

Pre-authorization and deposit compliance

Pre-authorization is the process of placing a hold on a guest’s card at check-in to cover the estimated stay cost plus incidentals. This is not a charge. It is a temporary hold that must be released or converted to a final charge within a defined window. Card network rules for lodging merchants allow estimated authorizations that include a buffer for incidentals, typically 15% above the room rate for Visa and Mastercard transactions.

Incremental authorizations allow you to add to an existing hold when a guest extends their stay or incurs additional charges. No-show charges require a separate authorization and must align with your disclosed cancellation policy. Failing to follow these network rules exposes you to chargebacks that are nearly impossible to win.

Chargeback mitigation through billing clarity

Chargeback risk in motels is directly linked to unclear billing and poor cancellation dispute management. The most effective defense is a billing descriptor that clearly identifies your property name, city, and contact number on the guest’s card statement. Guests who cannot recognize a charge dispute it immediately. Digital documentation, including signed registration cards, email confirmations, and timestamped check-in records, forms the evidence package you need for representment.

- Use a billing descriptor that matches your property’s public-facing name exactly.

- Collect digital signatures on registration cards at check-in.

- Send email confirmations that include your cancellation policy in plain language.

- Store all transaction records for a minimum of 18 months to cover dispute windows.

- Respond to chargeback notices within the processor’s required timeframe, typically 7 to 10 business days.

Using multiple Merchant IDs for multi-segment motels

Segmenting payment infrastructure with multiple Merchant IDs helps multi-property or multi-revenue motels manage compliance and risk separately. A motel with a restaurant, a pool bar, and room bookings benefits from separate MIDs for each revenue stream. This isolates chargeback ratios by segment, prevents a spike in food and beverage disputes from affecting your lodging MID, and simplifies reconciliation. The trade-off is that separate MIDs require proactive liquidity monitoring to avoid settlement delays across accounts.

Pro Tip: Ask your acquirer to assign MCC 7011 (Hotels and Motels) to your primary lodging MID. Using the correct MCC qualifies your transactions for lodging-specific interchange rates, which are typically lower than general retail rates for card-present transactions.

How can motels optimize payment security and customer experience?

Securing payment data and delivering a frictionless guest experience are not competing goals. The right technology choices accomplish both simultaneously, and the path forward is clearer than most motel operators realize.

Tokenization and third-party gateways

Tokenization replaces a guest’s actual card number with a unique, non-sensitive token that your system stores instead of the Primary Account Number (PAN). When you use a PCI DSS validated payment gateway like Stripe, Braintree, or a processor-provided hosted payment page, the gateway handles tokenization and your PMS never sees raw card data. This single change can move you from SAQ D to SAQ A, as noted earlier, and reduces your PCI compliance scope to the smallest possible footprint.

Automated re-authorization workflows

Card holds expire. Credit card authorizations typically expire after 2 days, and debit card holds expire after 4 days. Automated re-authorization systems refresh these holds before expiry, preventing the front desk from discovering at checkout that a guest’s card hold has lapsed. This is especially critical for extended stays and for motels with high debit card usage. Modern property management systems and payment gateways offer automated re-authorization as a standard feature. If yours does not, that is a gap worth addressing before your next busy season.

Here is a step-by-step approach to building a payment security framework for your motel:

- Audit your current card data flow. Map every point where card data enters, moves through, or is stored in your systems, including your PMS, booking engine, and front desk terminal.

- Outsource card data storage. Move to a tokenized, hosted payment page or gateway so your systems never store raw PANs.

- Inventory all third-party scripts on your booking page. Document each script’s source, purpose, and integrity hash to satisfy PCI DSS v4.0.1 script integrity requirements.

- Enable MFA on all administrative access points. This includes your PMS, payment gateway dashboard, and any cloud-based management tools.

- Train front desk staff on PCI awareness. Staff should know never to write down card numbers, how to recognize social engineering attempts, and what to do if a suspected breach occurs.

- Document your incident response plan. A one-page procedure covering who to call, what to preserve, and how to notify guests is sufficient for most Level 4 motels.

| Security Measure | Compliance Benefit | Guest Experience Benefit |

|---|---|---|

| Tokenization | Reduces PCI scope to SAQ A | Faster checkout, no card re-entry |

| Hosted payment page | Removes PMS from card data scope | Consistent, branded booking flow |

| Automated re-authorization | Prevents hold expiry disputes | No surprise declines at checkout |

| MFA on admin access | Meets PCI DSS v4.0.1 mandate | Protects guest data from breaches |

| Script integrity checks | Satisfies PCI DSS v4.0.1 requirement | Reduces booking page load risk |

Pro Tip: When evaluating lodging payment processing solutions, ask vendors specifically whether their integration removes your PMS from PCI scope. A vendor who cannot answer that question directly is not the right partner for a compliance-focused motel operation.

Key takeaways

Motel credit card processing compliance requires PCI DSS alignment, 2026 regulatory adherence, and lodging-specific payment practices working together to protect revenue and guest data.

| Point | Details |

|---|---|

| PCI DSS SAQ selection matters | Moving from SAQ D to SAQ A cuts compliance questions from 300 to 22 and reduces annual costs significantly. |

| 2026 regulations carry real penalties | Dual-routing for debit and interchange fee rules on taxes took effect July 1, 2026, with $1,000 per-transaction fines for violations. |

| Chargeback defense starts at billing | Clear billing descriptors, digital signatures, and stored records are your strongest tools against dispute losses. |

| Tokenization shrinks your risk surface | Outsourcing card data storage to a validated gateway removes your PMS from PCI scope entirely. |

| Automated re-authorization prevents revenue loss | Refreshing card holds before expiry eliminates checkout declines on extended stays and debit transactions. |

What I’ve learned about motel compliance that most guides won’t tell you

Most compliance articles for motels treat PCI DSS as a checkbox exercise. The reality is that the biggest compliance failures I see are not technical. They are operational. A motel can have a perfectly tokenized payment gateway and still rack up chargebacks because the front desk staff wrote a card number on a sticky note to “help a guest over the phone.”

The 2026 regulatory changes, particularly the Regulation II dual-routing expansion and the interchange fee restrictions on taxes, are genuinely significant. But they are also manageable if you address them with your processor before a compliance review forces the conversation. The motels that struggle are the ones that wait for their acquirer to flag a problem rather than asking the right questions proactively.

One insight that surprises many operators: managing chargebacks effectively delivers more measurable revenue protection than adopting new payment technologies like e-wallets or tap-to-pay. A motel losing 1.5% of revenue to unwinnable chargebacks because of vague billing descriptors will not recover that loss by adding Apple Pay. Fix the fundamentals first.

The other underappreciated risk is the booking page script problem. Motels often believe that using a third-party booking engine means they have no PCI responsibility for that page. Under PCI DSS v4.0.1, if your website loads any third-party JavaScript on a page that leads to payment, you own the script inventory and integrity verification requirement. That includes your Google Analytics tag, your live chat widget, and your review platform badge. Most motel operators have never audited these scripts. That audit should happen this quarter.

— Jonathan

How Merchantsolutionscorp supports compliant motel payment processing

Merchantsolutionscorp works with motel and lodging operators across the US to build payment processing setups that meet PCI DSS requirements, support 2026 regulatory mandates, and reduce the operational burden on your front desk team. The platform offers motel-ready payment processing with tokenized card handling, dual-pricing options to offset processing fees, and POS systems configured for lodging environments. Free hardware programs with $0 upfront options mean you can upgrade your payment infrastructure without a capital outlay. Whether you are managing a single property or multiple locations with separate MIDs, Merchantsolutionscorp provides the setup, onboarding, and ongoing support to keep your payments secure and compliant from day one.

FAQ

What PCI DSS level applies to most independent motels?

Most independent motels qualify as PCI DSS merchant Level 3 or Level 4 based on annual transaction volume. Level 4 covers properties processing fewer than one million total card transactions per year.

What changed for motel debit card processing in 2026?

Starting July 1, 2026, US merchants including motels must offer at least two unaffiliated debit card networks for online transactions under the expanded Regulation II dual-routing requirement. Motels that do not support this through their payment processor are out of compliance.

How does tokenization reduce PCI compliance burden for motels?

Tokenization replaces raw card numbers with non-sensitive tokens, removing your PMS and local systems from PCI scope. This can reduce your SAQ from the 300-question SAQ D to the 22-question SAQ A, cutting compliance costs and audit time significantly.

What is the penalty for charging interchange fees on tax amounts in 2026?

The 2026 interchange fee prohibition carries a penalty of $1,000 per transaction for merchants that incorrectly apply fees to tax or gratuity amounts. Motels must confirm their payment systems transmit tax line items separately in transaction data.

How should motels defend against chargebacks?

Motels defend chargebacks most effectively through clear billing descriptors that match the property’s public name, digital signatures on registration cards, email confirmations with cancellation policies, and transaction records stored for at least 18 months.