Small Business Loans in Miami: 2026 Comparison Guide for Local Owners

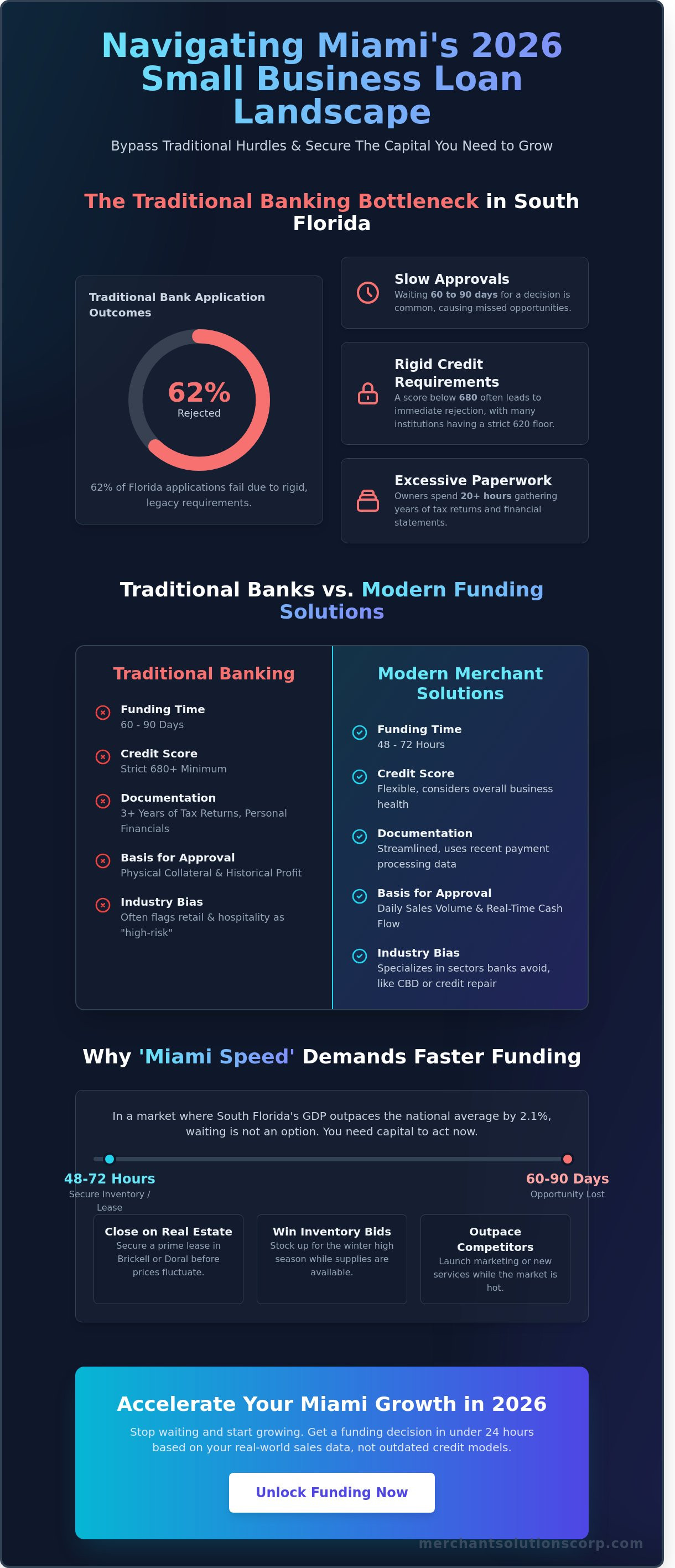

A credit score below 680 shouldn't be a death sentence for your Magic City expansion plans, yet 62% of traditional Florida bank applications still hit a wall due to rigid legacy requirements. You already know that waiting weeks for a "maybe" from a big bank is time your business simply doesn't have. Securing small business loans Miami owners can actually use requires moving past the slow-moving bureaucracy of traditional institutions. You need a partner who understands that a high-risk label for a CBD or credit repair business shouldn't stop your momentum.

We've streamlined the process to help you find the fastest, most cost-effective funding solutions available in 2026. This guide breaks down how to bypass strict credit barriers and secure the capital you need within 48 to 72 hours. You'll learn how to identify a loan that scales naturally with your revenue and connects you with a local Miami partner who prioritizes your growth. We'll compare the top lending landscapes so you can optimize your cash flow and future-proof your success.

Key Takeaways

- Navigate the shifting 2026 financial landscape by identifying the critical differences between traditional bank loans and agile alternative lending options.

- Unlock exclusive local capital by exploring updated public resources like the RISE Miami-Dade program and initiatives specifically for minority and women-owned businesses.

- Compare the mechanics of Merchant Cash Advances (MCA) and revenue-based financing to find the best-fit small business loans Miami provides for your cash flow needs.

- Streamline your decision-making process by using your current payment processing data to accurately assess your business's real-world funding capacity.

- Discover how integrating your financing with advanced POS technology can optimize your operations and safeguard your long-term scalability.

The 2026 Miami Small Business Loan Landscape: Beyond Traditional Banking

Miami's 2026 economy is moving at a breakneck pace. South Florida's GDP growth outpaced the national average by 2.1% in late 2025, creating a massive surge in demand for capital. This growth means that small business loans Miami entrepreneurs need must be accessible and flexible. Traditional commercial banks often lag behind this rapid expansion. They require mountains of paperwork and weeks of review. Alternative lenders have stepped in to fill this gap by offering a streamlined path to funding. For a broader overview of small business financing, many owners now look toward debt structures that prioritize daily cash flow over static physical assets.

To better understand how the local government is supporting this growth, watch this report on recent initiatives in the city:

The Small Business Administration (SBA) remains a cornerstone in the Miami-Dade ecosystem. However, the reality of SBA 7(a) loans is that they often take 60 to 90 days to fund. While these loans offer lower interest rates, they don't always fit the "Miami Speed" required to secure a prime storefront in Wynwood or restock inventory before the winter high season. Consequently, the 2026 landscape is defined by a shift in power. While Big Banks still hold roughly 45% of total loan volume, their market share is shrinking as local owners choose agile merchant solutions to bridge their financial gaps.

The "Miami Speed" Factor: Why Timing Matters in 2026

In 2026, a 90 day wait for a bank approval is often a death sentence for growth. Real estate prices in Brickell and Doral fluctuate monthly; if you can't close on a lease or buy inventory within 72 hours, you lose the opportunity to a competitor. Modern merchant solutions use data driven models to accelerate this process. They analyze your daily sales volume through advanced systems like Clover instead of just looking at your personal residence as collateral. This shift allows for approvals in under 24 hours, giving you the liquidity to act while the market is hot.

Common Barriers to Funding for South Florida Merchants

Credit scores remain a major bottleneck for many. Most local credit unions maintain a strict 620 floor for any commercial product. If your score is 615, your application is typically rejected immediately. Industry bias also persists in traditional circles. Banks often flag hospitality and retail as high risk sectors, which is a significant problem in a city where over 30% of the local economy relies on tourism and service. Documentation fatigue is another silent killer. The typical traditional application requires three years of tax returns and personal financial statements. Many Miami owners report spending 20+ hours gathering paperwork, only to be told their industry is no longer being funded.

- Credit Hurdles: Strict 620 minimums at traditional institutions.

- Sector Bias: Difficulty securing funds for "high-risk" hospitality or retail businesses.

- App Fatigue: Excessive documentation requirements that pull owners away from their daily operations.

Public and Non-Profit Funding: Miami-Dade County Resources

Miami entrepreneurs often overlook county-backed initiatives when searching for small business loans Miami. These programs prioritize local economic stability over high-profit margins. By utilizing public funds, you bypass the aggressive interest rates typically found in the private market. While SBA loan programs provide a national safety net, Miami-specific funds offer targeted relief for costs unique to South Florida. This section breaks down the most effective local alternatives to traditional banking.

The RISE Program: Pros, Cons, and Eligibility

The RISE Miami-Dade Small Business Loan program entered 2026 with refreshed capital reserves to support local growth. It targets businesses with fewer than 50 employees and less than $5 million in annual revenue. The application process requires a clear debt-to-income ratio and a detailed use-of-funds statement. You can secure up to $75,000 to cover operational gaps or expansion costs.

Eligibility hinges on your Sunbiz registration. You must demonstrate at least two years of active history in Florida. This non-negotiable benchmark proves your business has survived the initial startup phase. The most attractive feature is the "Prime minus 1%" interest rate. This means if the prime rate is 8%, your loan costs only 7%. It significantly lowers your monthly overhead, allowing you to reinvest that cash back into your team or marketing. Managing your monthly cash flow becomes even more predictable when you pair these low-interest funds with transparent payment processing pricing that eliminates hidden surcharges.

The Florida Small Business Development Center (SBDC) at FIU acts as the gateway for these applications. They provide no-cost technical assistance to help you prepare financial statements. Don't apply until an SBDC consultant reviews your package; their 90% success rate with prepared applicants is worth the extra week of preparation.

CDFI Loans: Funding for Underserved Miami Communities

Community Development Financial Institutions (CDFIs) bridge the gap for owners who don't meet strict commercial credit scores. These are mission-driven lenders that receive federal tax credits to lend in specific zip codes. In Miami, the Miami Bayside Foundation (MBF) stands out as a premier CDFI. They require 51% minority or women ownership and a physical domicile within Miami-Dade County.

- Working Capital: Use funds to bridge seasonal dips in tourism-heavy months like August and September.

- Inventory: Secure bulk pricing for retail goods before the winter peak season.

- Equipment: Finance specialized ovens for bakeries or lifts for auto shops without high-interest leases.

CDFIs offer more flexibility than banks but require more reporting. You'll likely need to provide quarterly financial updates to prove the loan is creating local jobs. This accountability ensures the capital stays within the community, fostering long-term resilience for Miami's diverse business owners.

Alternative Financing Comparison: MCA vs. Revenue-Based Loans

Miami’s fast-paced economy often demands capital faster than a traditional bank can move. While many owners search for small business loans Miami, they frequently find that alternative financing fits their operational reality better. A Merchant Cash Advance (MCA) isn't technically a loan. It's a commercial transaction where a provider purchases a portion of your future credit card sales at a discount. You receive a lump sum upfront, and the provider collects a fixed percentage of your daily receipts until the obligation is met.

Revenue-based financing operates on a similar logic but typically evaluates your total gross revenue across all channels. Both models prioritize your current cash flow over a perfect credit score. To streamline this process, ACH and eCheck processing allows for automated, friction-free repayments. This technology ensures that the daily or weekly pulls happen behind the scenes, so you don't have to manage manual transfers or worry about missing a deadline.

Merchant Cash Advances (MCA): Speed Over Interest Rates

Speed is the primary driver for MCAs. For the thousands of restaurants and seasonal retailers in the Miami-Dade area, equipment failure or a sudden surge in tourism requires immediate liquidity. Most MCA providers offer a 24-48 hour approval window. You can access funds while competitors are still gathering three years of tax returns for a traditional bank application.

It's vital to understand factor rates instead of APR. A factor rate of 1.2 or 1.4 is common. If you take $50,000 with a 1.2 factor rate, you'll pay back $60,000. Unlike an amortizing loan, the cost is fixed. You won't save money by paying early, but you gain the agility to capitalize on immediate inventory discounts or emergency repairs that could otherwise halt your operations.

Revenue-Based Financing: The Flexible Alternative

Revenue-based financing offers a safety net during Miami’s predictable seasonal shifts. In slower months like September or October, your payments decrease because they're a fixed percentage of your actual sales. If your POS data shows a dip, your repayment amount drops automatically. This protects your operating capital when foot traffic at your Wynwood gallery or South Beach boutique is lower than usual.

This model relies heavily on your real-time POS data to determine borrowing power. Because the lender's success is tied directly to your sales performance, they typically don't require physical collateral like real estate or personal assets. It's a performance-based solution that scales with your growth. This flexibility makes it a top choice for businesses looking for small business loans Miami alternatives that won't strain their cash flow during the off-season.

Selection Guide: Matching Your Miami Business to the Right Loan

Securing small business loans Miami requires a strategy tailored to your specific industry lifecycle. A startup in Wynwood has different capital needs than an established distributor in Doral. You must align your debt with your actual cash flow. One of the most effective ways to determine your borrowing limit is by analyzing your payment processing pricing. This data reveals your true margins after all transaction costs are settled. Lenders in 2026 prioritize businesses that demonstrate this level of financial granularity.

You should also consider how your revenue model affects your eligibility. For instance, implementing dual pricing and cash discounts can significantly boost your bottom line. By offsetting credit card fees, you increase your net income. This higher profit margin makes your business a safer bet for banks and alternative lenders alike. It's a simple way to future-proof your debt while ensuring you don't overextend your monthly obligations.

Financing for High-Risk Miami Industries

Miami is a hub for specialized sectors like CBD, Kratom, and credit repair. These businesses often face rejection from traditional banks. The challenge usually stems from "frozen funds" or sudden account closures that disrupt the repayment of small business loans Miami. You can mitigate these risks by securing a high-risk merchant account first. These specialized accounts provide the transparent transaction history lenders need to see. Data from 2025 indicates that high-risk businesses with stable processing histories are 25% more likely to secure private funding than those using generic, non-specialized processors.

Hospitality and Retail: Leveraging POS for Better Terms

For Miami's vibrant restaurant and retail scene, your hardware is a financial asset. Clover POS systems do more than take payments; they generate the real-time inventory and sales reports that lenders love. Instead of guessing your growth potential, you can show a lender exact peak-hour volume and stock turnover rates. This level of detail reduces the perceived risk for the financier.

Consider a North Miami cafe that wanted to expand in early 2025. By using POS-integrated data, they proved a 15% month-over-month growth in their morning rush. This transparency allowed them to secure an expansion loan with a 2% lower interest rate than the local average. They didn't just get a loan; they leveraged their data to get better terms. If you want to scale, your data must tell a story of consistency and control.

Ready to optimize your cash flow before applying for your next loan? Review our transparent pricing plans to see your true margins.

How Merchant Solutions Corp Accelerates Your Growth in Miami

Miami's economic landscape in 2026 requires more than a generic lender. It demands a local partner who understands the high-velocity Florida market. Merchant Solutions Corp provides a solution-oriented approach to capital, focusing on your business's actual performance rather than outdated metrics. Based in North Miami, we've helped local entrepreneurs scale by providing the liquidity they need without the red tape of traditional banks. When you're searching for small business loans Miami experts can provide, you need a team that knows the difference between a seasonal dip and a long-term trend. We know that a business in Wynwood has different needs than one in Aventura. Our team lives and works in this community, giving us a unique perspective on the growth opportunities specific to South Florida.

We handle the heavy lifting regarding security and compliance. You shouldn't spend your nights worrying about PCI DSS standards or fraud prevention. We implement advanced tokenization and P2P encryption, allowing you to focus on scaling your operations while we safeguard your transactions. This proactive security posture reduces your liability and builds trust with your customer base. You focus on the guest experience; we'll handle the back-end complexity that often slows down growing enterprises.

Seamless Integration: Payment Processing Meets Capital

Your merchant account serves as the most accurate pulse of your business health. While banks look at tax returns from two years ago, we look at your current cash flow. By using advanced POS systems, we turn your daily sales data into a powerful tool for securing small business loans Miami owners can use for immediate expansion. This future-proof approach ensures your technology and your capital grow at the same pace. Merchant Solutions Corp streamlines the path from application to funding by integrating your payment data directly into the underwriting process.

Get Started: Your Road Map to Funding

Securing capital shouldn't feel like a second job. Our 3-step consultation process is designed for speed. First, we conduct an initial discovery to review your current processing volume and growth goals. Second, we tailor a funding structure that fits your specific industry, whether you're in hospitality, retail, or a high-risk sector. Finally, we move to rapid activation where funds are deployed to your account to fuel your next project.

To keep the process moving, have your last four months of bank statements, your processing history, and a clear growth plan ready for our team. We don't just provide a check; we provide a strategic partnership built on transparency and reliability. Schedule a call with our Miami experts today to see how we can help you dominate the local market.

Empower Your Growth in the 305

Navigating the complex landscape of small business loans Miami entrepreneurs face in 2026 requires more than just a basic bank application. You've seen how Miami-Dade County's 2025 program expansions and the shift toward revenue-based financing have redefined capital access for local owners. Success depends on matching your specific industry needs, whether you're in the hospitality sector or a high-risk niche, with a funder that understands local market dynamics. Relying on outdated lending models won't work when speed and flexibility are the new standards for scaling.

Merchant Solutions Corp provides the edge you need with our local North Miami office where you can get face-to-face support. We specialize in tailored solutions for high-risk and hospitality sectors that traditional lenders often overlook. Our systems feature integrated POS and payment processing to make repayment seamless and automated. It's time to future-proof your operations with a partner that's invested in South Florida's success.

Apply for Fast Miami Small Business Funding Now

Your next chapter of expansion starts with the right capital partner. We're ready to help you scale.

Frequently Asked Questions

How long does it take to get a small business loan in Miami?

Funding timelines depend on the specific lender you choose for your capital needs. Traditional banks in South Florida typically require 30 to 90 days to process the small business loans Miami entrepreneurs apply for. If you need capital faster, alternative lenders often provide approval within 24 hours and deposit funds in 48 hours. This speed allows you to optimize your operations without waiting months for a committee decision.

What is the minimum credit score for a small business loan in Florida?

Most traditional banks in Florida require a minimum FICO score of 680 for standard commercial loan approval. SBA 7(a) loans generally look for scores above 640 to meet their federal credit requirements. If your score is lower, alternative financing options like merchant cash advances accept scores as low as 500. These programs focus more on your monthly revenue than your personal credit history to determine eligibility.

Can I get a business loan in Miami if my business is considered high-risk?

You can secure funding even if your industry is labeled high-risk by traditional financial institutions. Specialty lenders in Miami focus on sectors like cannabis, credit repair, and debt collection that big banks often avoid. These providers use customized underwriting to streamline the approval process for businesses with higher chargeback rates. This approach ensures you get the capital needed to safeguard your business against unpredictable market fluctuations.

What is the difference between the RISE Miami-Dade loan and a private MCA?

The RISE Miami-Dade Fund offers low-interest term loans up to $30,000 with fixed monthly payments for local small businesses. A private Merchant Cash Advance (MCA) differs because it's not a loan but a purchase of your future sales. MCAs provide faster access to cash but involve daily or weekly remittances based on your credit card volume. This makes MCAs more flexible for businesses with seasonal revenue shifts.

How do I apply for the Miami Bayside Foundation loan program?

To apply for a Miami Bayside Foundation loan, you must submit an online application through their official portal. You'll need to provide two years of federal tax returns, six months of business bank statements, and a detailed business plan. This foundation specifically targets minority-owned businesses within the City of Miami limits. Their team reviews applications to provide tailored financial assistance that helps local owners scale their operations effectively.

What documents are required for a fast merchant cash advance in Miami?

Getting small business loans Miami owners use for quick cash, such as an MCA, requires minimal paperwork compared to bank loans. You generally only need to provide the last four months of business bank statements and your most recent tax return. Lenders also require a copy of your driver's license and a voided business check to facilitate the wire transfer. This simplified documentation helps you skip the hassle of traditional bank requirements.

Are there small business grants available in Miami-Dade County for 2026?

Miami-Dade County continues to offer the Mom and Pop Small Business Grant, which provides up to $5,000 for qualifying local shops. The BizUp Miami program also offers grants and technical assistance to startups in underserved communities throughout 2026. You should check the Miami-Dade Economic Advocacy Trust website for specific application windows and eligibility criteria. These programs offer a secure way to fund equipment or marketing without taking on debt.

How does revenue-based financing affect my daily cash flow?

Revenue-based financing adjusts your repayment amounts based on your daily sales volume rather than a fixed monthly schedule. When your sales increase, the payment amount rises; when sales slow down, the payment decreases proportionally. This structure protects your cash flow during quiet periods, ensuring you don't face a fixed debt burden you can't afford. It's a cutting-edge way to align your financing costs directly with your actual business performance.