Why Lower Payment Fees Matter for Small Businesses

Why Lower Payment Fees Matter for Small Businesses

Payment processing fees are the percentage-based and fixed costs that card networks, banks, and processors charge every time a customer pays by credit or debit card. For small businesses operating on tight margins, these fees are not a minor line item. US businesses paid over $187 billion in card fees in 2024, and that number continues to climb. Understanding why lower payment fees matter is the first step toward protecting your revenue, pricing competitively, and keeping more of what you earn. This guide breaks down how fees work, where they hit hardest, and what you can do about them in 2026.

Why lower payment fees matter for your bottom line

Payment processing fees typically fall into three layers: interchange, assessments, and processor markup. Interchange is the largest portion, paid to the card-issuing bank. Assessments go to the card networks, Visa and Mastercard. Processor markup is what your payment processor adds on top. Together, these layers create your effective rate.

Processing fees for small businesses typically range from 2.5% to 3.5%, with e-commerce and high-risk merchants paying up to 8%. That range matters because a 1% difference on $500,000 in annual card revenue equals $5,000 in additional costs. That is money that could cover payroll, inventory, or marketing.

The impact of payment fees on profits is not theoretical. It is measurable on every statement. A retail shop processing $30,000 per month at 3.0% pays $900 in fees. Drop that rate to 2.5% and the savings reach $1,800 per year without changing a single product or adding a single customer.

How fee structures differ by industry

Different business types face different fee environments. Here is a realistic view of what merchants across industries pay:

| Business Type | Typical Effective Rate | Key Fee Driver |

|---|---|---|

| Retail (card present) | 2.5%–3.0% | Interchange on card type |

| Restaurant | 2.5%–3.2% | Card mix, tips processing |

| E-commerce | 2.8%–3.8% | Card-not-present surcharge |

| High-risk merchants | 4.0%–8.0% | Risk premium, chargeback exposure |

| Coffee shop / low ticket | 3.5%–5.0% | Per-transaction flat fee impact |

High-risk industries face the steepest rates because processors price in the cost of potential chargebacks and fraud. E-commerce merchants pay more because card-not-present transactions carry higher fraud risk. Understanding where your business sits in this table tells you how much room you have to negotiate.

Pro Tip: Request an itemized breakdown of your current statement. Most processors bundle interchange, assessments, and markup into a single line. Separating them reveals exactly where your money is going.

Beyond base rates, PCI compliance and chargeback management add fixed and variable costs that can reach thousands of dollars annually. These hidden costs inflate your true effective rate well beyond the advertised percentage.

How do payment fees influence pricing and cash flow?

Every percentage point in fees reduces your net revenue directly. If your gross margin on a product is 30% and your payment fee is 3%, fees consume 10% of your margin before you account for any other operating cost. That relationship between fee percentages and net revenue is the core reason the benefits of lower payment fees extend far beyond the fee line itself.

Consider a restaurant with a $25 average ticket. At 3.2%, the fee per transaction is $0.80. That same restaurant serving 200 covers per day pays $160 in daily processing fees, or roughly $58,400 per year. Reducing the effective rate to 2.7% saves over $18,000 annually. That is a part-time employee, a new piece of equipment, or a meaningful addition to cash reserves.

“Merchant fees, while often dismissed as the cost of doing business, can quietly erode margins and must be tracked monthly to avoid unnecessary costs.” — US Chamber of Commerce

The cash flow effects are equally significant. Fees are deducted before funds settle into your account. For businesses with thin margins or seasonal revenue, that daily deduction compounds quickly. A lower transaction cost means more working capital available for day-to-day operations without relying on credit lines.

The hidden cost of funding consumer rewards

Higher interchange fees fund consumer rewards programs, meaning merchants effectively subsidize cashback and travel points for cardholders. Premium rewards cards carry interchange rates significantly above standard cards. When a customer pays with a premium Visa Infinite or Amex Platinum card, your effective rate rises automatically. This is a cost you absorb unless your pricing accounts for it.

The practical response is to build fee awareness into your pricing strategy. E-commerce merchants, in particular, benefit from reviewing pricing strategies for online businesses that account for card mix and fee variability across transaction types.

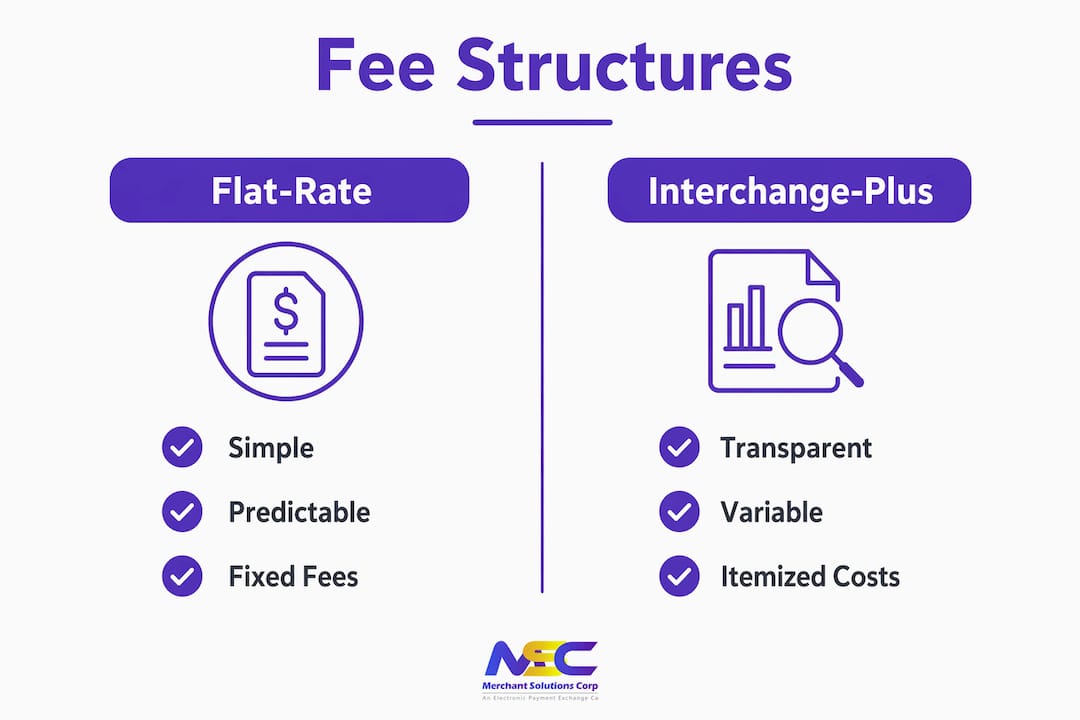

How can businesses compare fee models and choose the right processor?

The two dominant pricing models are flat-rate and interchange-plus. Each has a different risk and reward profile depending on your average transaction size and card mix.

Flat-rate pricing charges a single percentage plus a fixed fee per transaction, regardless of card type. This model is simple and predictable. It works well for low-volume businesses or those just starting out. The downside is that the processor bundles its margin into the rate, and you have no visibility into what portion is markup.

Interchange-plus pricing separates the processor’s markup from the underlying interchange and assessment costs. Processor markup typically accounts for 20–25% of total transaction costs and is the negotiable portion. Interchange-plus gives you full transparency and the ability to negotiate the markup independently.

Flat-rate vs. interchange-plus: a direct comparison

| Factor | Flat-Rate | Interchange-Plus |

|---|---|---|

| Transparency | Low | High |

| Predictability | High | Moderate |

| Best for | Low volume, simple operations | Medium to high volume |

| Negotiability | Limited | Strong |

| Effective cost at scale | Higher | Lower |

The average ticket size determines which model saves you more money. A $5 transaction at a flat rate of $0.10 plus 2.6% carries an effective rate of 4.6%. The same processor’s rate on a $100 transaction drops to 2.7%. This regressive effect hits coffee shops, food trucks, and quick-service restaurants hardest.

Pro Tip: Calculate your average ticket size before choosing a pricing model. If your average transaction is under $15, negotiate the per-transaction flat fee down aggressively. That fixed cost matters more than the percentage rate at low ticket sizes.

Steps to evaluate and choose a processor

- Pull three months of processing statements and calculate your true effective rate (total fees divided by total volume).

- Request interchange-plus quotes from at least three processors.

- Compare the markup component directly, not the advertised rate.

- Ask each processor to itemize all monthly fees: PCI compliance, gateway fees, statement fees, and batch fees.

- Confirm whether the processor offers volume-based rate reductions as your business grows.

Negotiating payment processing fees requires confidence and preparation. Processors expect negotiation. Arriving with competitive quotes and your actual volume data puts you in a strong position.

What practical steps reduce payment processing fees?

Reducing fees is not a one-time task. It requires a consistent process built into your monthly financial review. The following steps represent the most direct ways to lower transaction costs and improve your net revenue.

-

Audit your merchant statement monthly. Regular auditing of merchant statements helps identify hidden fees, duplicate charges, and incremental cost increases from assessment changes. Many businesses pay fees they never agreed to simply because no one reviewed the statement.

-

Request competing quotes annually. The payment processing market is competitive. Benchmarking your current rate against three competing offers every 12 months gives you negotiating leverage and market awareness.

-

Encourage debit and ACH payments. Regulated debit interchange is approximately 0.05% plus $0.21, a fraction of standard credit card rates. Posting a small sign at checkout or training staff to mention debit as an option can meaningfully shift your card mix over time.

-

Explore dual pricing or surcharging. Where legally permitted, passing the cost of credit card processing to customers who choose to pay by card is a direct way to offset fees. Merchantsolutionscorp offers dual pricing solutions specifically designed for this purpose, with compliant signage and automatic rate adjustments built into the POS system.

-

Leverage transaction volume for better rates. Businesses processing $100,000 or more per month qualify for volume-based interchange-plus rates that are not available to low-volume merchants. If you are approaching that threshold, use it as a negotiating point before you reach it.

-

Reduce chargebacks proactively. Chargebacks trigger fees, processor penalties, and in some cases, rate increases. Clear return policies, accurate product descriptions, and fast customer service reduce dispute rates and protect your processing costs.

Pro Tip: When negotiating, do not focus only on the percentage rate. Ask processors to waive or reduce monthly fees like PCI compliance fees ($9.95–$19.95/month), statement fees, and gateway fees. These fixed costs add up to hundreds of dollars per year regardless of your volume.

Key takeaways

Lower payment fees directly protect profit margins, improve cash flow, and give small businesses the financial flexibility to grow without raising prices.

| Point | Details |

|---|---|

| Fees compound quickly | A 0.5% rate reduction on $500,000 in annual volume saves $2,500 per year. |

| Interchange-plus wins at scale | Transparent pricing models allow negotiation and reduce effective rates for medium and high-volume businesses. |

| Ticket size changes everything | Low-ticket businesses must negotiate per-transaction flat fees, not just percentage rates. |

| Monthly audits catch hidden costs | Regular statement reviews identify fees that can be challenged, removed, or renegotiated. |

| Debit and ACH lower your cost | Shifting even a portion of transactions to debit or ACH meaningfully reduces your overall processing expense. |

The fee conversation most business owners avoid

Most small business owners accept payment processing fees the way they accept rent. They treat it as fixed, unavoidable, and not worth the effort to challenge. That mindset is expensive.

The reality is that processor markup is negotiable. Processors often bundle non-negotiable interchange and assessments with their own margin to obscure the true cost. When you cannot see the markup, you cannot challenge it. Demanding an interchange-plus quote is not aggressive. It is standard financial due diligence.

The second misconception is that only large businesses have leverage. Volume matters, but so does preparation. Walking into a negotiation with three competing quotes, your actual processing volume, and a clear understanding of interchange-plus pricing puts even a small retailer in a credible position. Processors would rather reduce their markup slightly than lose the account entirely.

The long-term impact of fee management is not just about saving money today. It is about building a business with healthier margins that can absorb cost increases, invest in growth, and price competitively without squeezing profit. Businesses that treat payment fees as a managed expense rather than a fixed cost consistently outperform those that do not.

Start with your last three statements. Calculate your true effective rate. Then make one call to benchmark it against the market. That single action is where the financial savings from lower fees begin.

— Jonathan

How Merchantsolutionscorp helps you pay less to process more

Merchantsolutionscorp works with restaurants, retailers, and service businesses across the US and Canada to reduce processing costs through transparent pricing and industry-specific setups. The platform offers interchange-plus pricing, dual pricing solutions to offset credit card fees, and free hardware programs with $0 upfront costs. Whether you run a high-volume retail location or a specialty service business, Merchantsolutionscorp structures your payment processing setup around your actual transaction profile. You can also review competitive processing rates directly to see how your current costs compare. Getting started takes one conversation, and the savings show up on your very first statement.

FAQ

What are typical payment processing fees for small businesses?

Payment processing fees for US small businesses typically range from 2.5% to 3.5%, with e-commerce and high-risk merchants paying up to 8%. Your effective rate depends on card mix, average ticket size, and pricing model.

What is the difference between flat-rate and interchange-plus pricing?

Flat-rate pricing bundles all costs into one percentage for simplicity, while interchange-plus separates the processor’s markup from interchange and assessments. Interchange-plus pricing is more transparent and typically more cost-effective for businesses processing higher volumes.

How do payment fees affect cash flow for small businesses?

Fees are deducted before funds settle, reducing the working capital available each day. For low-margin businesses, even a 0.5% reduction in effective rate can free up thousands of dollars annually that would otherwise require a credit line to replace.

Can small businesses negotiate payment processing fees?

Yes. Negotiating fees is possible with preparation and competing quotes. The processor markup portion is negotiable, and businesses with consistent monthly volume have real leverage to request better terms.

What is the cheapest way to accept payments as a small business?

Encouraging customers to pay by debit card or ACH transfer reduces costs significantly. Regulated debit interchange runs approximately 0.05% plus $0.21 per transaction, far below standard credit card rates. Combining debit encouragement with interchange-plus pricing delivers the lowest effective rates for most small businesses.

Recommended

- Benefits of Zero Fee Payment Processing for Small Businesses | Merchant Solutions Corp

- Why Flat Rate Is a Good Program for Your Business | Merchant Solutions Corp

- Set up payment processing: a simple guide for small businesses | Merchant Solutions Corp

- Accept online payments: low-cost solutions for SMBs | Merchant Solutions Corp