ACH Payments in Legal Services: A 2026 Practice Guide

ACH Payments in Legal Services: A 2026 Practice Guide

ACH payments in legal services are defined as electronic, bank-to-bank transfers processed through the Automated Clearing House network, giving law firms a direct method to collect client payments without relying on checks or credit cards. The industry standard body governing these transfers is NACHA, which sets compliance rules for authorization, timing, and fund handling. ACH transaction costs typically range from $0.26 to $0.50 per transaction, compared to credit card fees that average 2.5–5.0%. That cost gap is significant for law firms processing large retainers or recurring monthly billing. As of 2026, 78% of individuals and 74% of businesses prefer electronic payments over traditional methods. That preference makes ACH adoption not just a cost decision but a client service decision. IOLTA compliance adds another layer of urgency, since law firms must correctly route funds between trust and operating accounts. ACH, when properly configured, supports that requirement directly.

How do ACH payments work in legal practice workflows?

ACH payment processing in a law firm follows a defined sequence that differs meaningfully from swiping a card at a retail counter. Understanding each step helps you build a workflow that stays compliant and reduces manual work.

The authorization and NACHA compliance requirement

Every ACH transaction begins with client authorization. NACHA rules require that authorization language be clear, specifying the payment amount, timing, and the account being debited. This authorization serves as the legal basis for the transfer and must be documented and retained. For law firms, this is not optional. A missing or vague authorization creates both a compliance gap and a dispute risk.

The authorization can be captured through a signed paper form, a client portal, or a secure online payment page. Client portals are the preferred method in 2026 because they create a digital record tied directly to the matter file. Integrating ACH into client portals connected to systems like Needles and Litify unifies authorization and payment records in one place. That integration eliminates the need to manually cross-reference payment records against billing entries.

The ACH transaction lifecycle and timing

Once authorization is captured, your processor submits the ACH file to the client’s bank through the Automated Clearing House network. ACH payments typically settle within 3–5 business days, with some banks offering same-day processing depending on submission cutoffs. That timeline is slower than a credit card authorization but faster than waiting for a paper check to clear. For retainer replenishment or monthly billing cycles, the predictable timing works in your favor.

The standard ACH lifecycle moves through these steps:

- Client authorization captured via client portal, signed form, or secure payment page.

- ACH file generated by your billing or payment platform and submitted to your bank.

- Bank forwards the file to the Automated Clearing House network for processing.

- Funds debited from the client’s account, typically within one business day of submission.

- Funds credited to your firm’s trust or operating account within 3–5 business days.

- Payment recorded in your billing software and matched to the open invoice or matter ledger.

- Return activity monitored for rejected transactions, insufficient funds, or closed accounts.

Pro Tip: Set up automated return monitoring alerts in your billing platform. Returned ACH transactions carry a return code that tells you exactly why the payment failed, which makes follow-up faster and more targeted than chasing a bounced check.

IOLTA compliance and account mapping

The most critical compliance step for law firms is accurate account mapping. Properly routing funds to trust versus operating accounts during ACH receipt is required for IOLTA compliance. A retainer payment goes to the trust account. A payment for earned fees goes to the operating account. Mixing these creates reconciliation problems and potential bar association violations. Your payment processor and billing software must both support separate account designations for each transaction type.

How do ACH payments compare to other law firm payment methods?

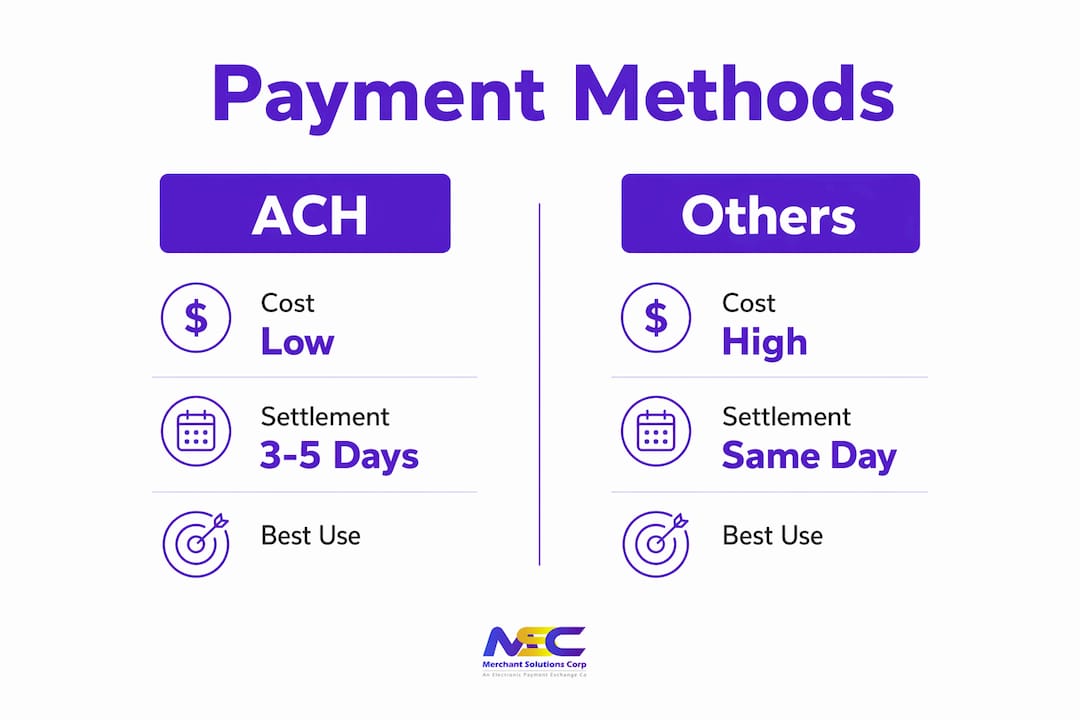

Law firms typically use four payment methods: paper checks, wire transfers, credit cards, and ACH. Each has a different cost profile, speed, and risk level. Understanding where ACH fits helps you decide which method to use for each billing scenario.

| Payment method | Typical cost | Settlement time | Best use case |

|---|---|---|---|

| Paper check | Near zero direct cost | 3–7 business days | Court filings, vendor payments |

| Wire transfer | $15–$50 per transaction | Same day to 1 business day | Large one-time payments |

| Credit card | 2.5–5.0% of transaction | 1–2 business days | Smaller invoices, client convenience |

| ACH | $0.26–$0.50 per transaction | 3–5 business days | Retainers, recurring billing, large invoices |

ACH wins on cost for any transaction above a few hundred dollars. A $5,000 retainer processed by credit card at 3% costs your firm $150 in fees. The same payment via ACH costs under $1.00. That difference compounds quickly across a full client roster.

Key considerations when choosing between payment methods:

- Recurring retainers: ACH is the clear choice. You capture authorization once and automate monthly debits without client action each cycle.

- Large invoices: ACH eliminates the percentage-based fee that makes credit cards expensive at high dollar amounts.

- Urgent same-day needs: Wire transfer remains the only reliable same-day option, though at a higher per-transaction cost.

- Client convenience for smaller amounts: Credit cards remain useful for initial consultations or small flat-fee matters where client preference outweighs cost.

- Fraud exposure: Checks carry the highest fraud risk among all payment methods. ACH transactions have defined dispute windows and return codes that make unauthorized transaction resolution more structured.

Checks remain prevalent in legal settings due to court and vendor requirements, but ACH is increasingly the standard for predictable, repeat payments. The two methods are not mutually exclusive. Most firms run both, using checks where required and ACH where efficiency matters most.

What are the benefits of ACH payments for law firms?

Adopting electronic ACH payments produces measurable gains across billing, collections, and compliance. The benefits are not theoretical. They show up in reduced administrative hours, lower processing costs, and faster cash flow.

Reduced administrative workload

Electronic payments platforms integrated with legal billing software improve trust account reconciliation and reduce manual data entry errors. When a payment posts automatically to the correct matter ledger, your billing staff does not need to manually match deposits to invoices. That reduction in manual work is especially valuable at month-end, when IOLTA reconciliation requires every trust account transaction to be accounted for precisely.

Lower processing costs and better cash flow

ACH costs of $0.26–$0.50 per transaction make it the most cost-efficient electronic payment method for law firms. Those savings are most significant on large invoices and recurring retainers where credit card fees would otherwise consume a meaningful portion of revenue. Faster collections also improve cash flow. Adopting electronic ACH payments reduces the billable partner time spent on collections, which accelerates revenue cycles and improves firm profitability.

Automation and error reduction

- Automated ACH file generation removes the manual step of preparing payment batches.

- Integrated client portals centralize authorization, payment tracking, and ledger updates in one system.

- Return activity alerts notify staff immediately when a payment fails, enabling faster follow-up.

- Recurring billing schedules eliminate the need for clients to initiate payment each cycle.

- Audit trails tied to matter files give you a complete payment history for every client without manual record-keeping.

Automation tools for ACH payments minimize errors such as late return activity reviews and inconsistent fund deposits. Each of those errors, left unaddressed, creates reconciliation problems that take hours to untangle.

Pro Tip: Configure your billing software to automatically apply ACH payments to open invoices in chronological order. This prevents aged receivables from accumulating and keeps your trust account ledger accurate without manual intervention.

How should law firms implement ACH payments securely?

Implementation is where most law firms either get ACH right or create problems they spend months fixing. A structured approach prevents the most common compliance and operational errors.

-

Choose a processor that integrates with your billing software. Your ACH processor must connect directly to your case management or billing platform. Processors that require manual file exports and imports create re-keying errors and delay payment posting. Look for direct integrations with platforms like Needles, Litify, or your firm’s existing billing system.

-

Map trust and operating accounts before processing a single transaction. Work with your processor to configure separate account designations for trust and operating funds. Test the mapping with a small transaction before going live. Failing to map accounts correctly creates reconciliation issues and potential IOLTA compliance risks that are difficult to unwind after the fact.

-

Build a compliant client authorization process. Your authorization form or portal page must meet NACHA requirements. Include the payment amount, frequency, account to be debited, and the client’s right to revoke authorization. Store signed authorizations in the client’s matter file. For recurring retainers, confirm that the authorization explicitly covers ongoing debits, not just a single payment.

-

Set up return monitoring and dispute protocols. Returned ACH transactions are a normal part of operations. What matters is how quickly you identify and respond to them. Configure your platform to send return alerts within 24 hours of a failed transaction. Establish a clear internal protocol for contacting clients, re-presenting payments where appropriate, and documenting each step.

-

Train billing and accounting staff on ACH workflows. Staff who understand the ACH lifecycle make fewer errors. Training should cover authorization requirements, account mapping rules, return code interpretation, and the firm’s internal reconciliation process. Refresher training is appropriate whenever your billing software or processor updates its ACH features.

-

Maintain secure data handling for bank account information. Client bank account numbers and routing numbers are sensitive data. Your processor should use encryption and tokenization to protect stored account information. Confirm that your processor meets current data security standards and that client account data is never stored in unprotected spreadsheets or email threads.

Key Takeaways

ACH payments give law firms the most cost-efficient path to electronic billing, with NACHA compliance, IOLTA-compatible account mapping, and integration with legal billing software forming the foundation of a working system.

| Point | Details |

|---|---|

| ACH cost advantage | Transactions cost $0.26–$0.50 each, far below the 2.5–5.0% charged by credit card processors. |

| NACHA authorization | Every ACH debit requires documented client authorization that meets NACHA standards. |

| IOLTA account mapping | Trust and operating accounts must be mapped separately before processing any transaction. |

| Integration is critical | Connecting ACH to billing platforms like Needles or Litify eliminates manual data entry and reconciliation errors. |

| Client preference | As of 2026, 78% of individuals prefer electronic payments, making ACH adoption a client service priority. |

Why ACH integration belongs at the center of your billing system

Most law firms treat ACH as a payment option they bolt on after everything else is set up. That approach creates the exact friction it was meant to eliminate. When ACH authorization happens outside your case management system, you end up with payment records in one place and matter records in another. Reconciliation becomes a manual exercise, and the compliance risk grows with every transaction that does not automatically post to the right account.

The firms that get the most out of ACH are the ones that embed it into the matter workflow from the start. Authorization is captured at intake, tied to the client file, and linked directly to the billing ledger. When a payment posts, it updates the trust account balance, closes the open invoice, and creates an audit trail without anyone touching a keyboard. That is not a technology luxury. It is what IOLTA compliance actually requires in practice.

The other observation worth making is that ACH is not a set-it-and-forget-it system. Return rates, authorization language, and processor integrations all change as your firm grows and as NACHA updates its rules. A quarterly review of your ACH workflow, including return activity rates, authorization form language, and account mapping accuracy, keeps you ahead of problems before they become bar complaints. The firms that treat ACH as a living part of their billing infrastructure consistently outperform those that configure it once and walk away.

— Jonathan

Merchantsolutionscorp ACH processing for law firms

Merchantsolutionscorp offers ACH and eCheck processing built for professional service firms that need reliable, low-cost electronic payment collection. The platform supports separate account designations for trust and operating funds, making IOLTA-compliant billing straightforward from day one. Processing costs stay well below credit card rates, and the system connects with legal billing workflows to reduce manual reconciliation. If your firm is ready to move client billing to a more efficient model, Merchantsolutionscorp provides the payment processing infrastructure to support it, with onboarding support and no upfront hardware costs on qualifying accounts.

FAQ

What is ACH payment processing for law firms?

ACH payment processing for law firms is the electronic transfer of client funds directly from a bank account to the firm’s trust or operating account through the Automated Clearing House network. It is governed by NACHA rules and requires documented client authorization before any debit occurs.

How long does an ACH payment take to settle?

ACH payments typically settle within 3–5 business days, with same-day ACH available through some banks depending on submission cutoffs. This timeline is slower than credit card processing but significantly more cost-efficient for large invoices and recurring retainers.

Are ACH payments IOLTA compliant?

ACH payments are IOLTA compliant when your processor correctly maps incoming funds to the designated trust or operating account. Incorrect account mapping creates reconciliation errors and potential compliance violations, so account configuration must be verified before going live.

How do I accept ACH payments in my law firm?

To accept ACH payments, choose a processor that integrates with your billing software, configure trust and operating account mapping, build a NACHA-compliant client authorization process, and set up return monitoring. Training billing staff on the full ACH lifecycle completes the implementation.

Why are ACH payments better than checks for law firms?

ACH payments reduce fraud exposure, eliminate manual deposit trips, and post automatically to billing ledgers when integrated with case management software. Checks remain necessary for court filings and some vendor payments, but ACH is more efficient and auditable for recurring client billing.

Recommended

- Credit card processing for attorneys: boost revenue & get paid faster | Merchant Solutions Corp

- Top 4 What Payment Solution Is Recommended to Lawyers Alternatives 2026 | Merchant Solutions Corp

- Save money on processing fees by offering ACH payments | Merchant Solutions Corp

- Best payment solutions for contractors: complete guide | Merchant Solutions Corp