Credit Card Processing in Healthcare: 2026 Guide

Credit Card Processing in Healthcare: 2026 Guide

Credit card processing in healthcare is the practice of handling patient payments securely and compliantly while protecting sensitive health information and keeping billing operations running without friction. Unlike retail or restaurant environments, healthcare payment processing operates under two overlapping regulatory frameworks: PCI DSS, which governs card data security, and HIPAA, which governs protected health information (PHI). Processors like Chase InstaMed and Square have built healthcare-specific solutions that address both standards, but selecting the right setup requires understanding how these rules interact with your workflows. This guide explains how the process works, what compliance actually demands, how HSA and FSA cards factor in, and what to look for when choosing among the best payment processors for healthcare.

How does credit card processing work in healthcare settings?

Credit card processing in healthcare follows the same five-stage cycle as any other industry, but each stage carries healthcare-specific nuances that affect cost, risk, and compliance.

The five stages of a healthcare payment transaction:

- Authorization. The patient presents a card at the front desk or submits payment online. The terminal or payment gateway sends a request to the card network (Visa, Mastercard, etc.), which checks the cardholder’s available balance or credit limit and returns an approval or decline code in seconds.

- Capture. Once the provider confirms the charge amount, the transaction is captured. In healthcare, this step is sometimes delayed because the final patient responsibility is not known until insurance adjudication is complete. Pre-authorizations hold funds temporarily while the claim processes.

- Batching. Captured transactions are grouped into a batch, typically at the end of the business day. Healthcare practices with high transaction volumes benefit from automated batch closing to reduce manual workload.

- Clearing and settlement. The batch is submitted to the acquiring bank, which routes each transaction through the card networks to the issuing banks. Funds are confirmed and moved.

- Funding. The acquiring bank deposits net funds into the provider’s account, usually within one to two business days. Reconciliation against the practice management system (PMS) or electronic health record (EHR) happens at this stage.

The distinction between card-present (CP) and card-not-present (CNP) transactions matters significantly in healthcare. Card-not-present payments carry higher fraud risk and typically higher processing rates than in-office card swipes or taps. Telehealth billing, phone-based collections, and patient portal payments all fall into the CNP category. Providers who process a high volume of post-visit billing by phone or email should factor this cost differential into their pricing model decisions.

Healthcare also introduces staged billing scenarios that most retail processors are not built to handle. A patient may pay a copay at check-in, receive an insurance adjustment, and then owe a remaining balance weeks later. Your payment system needs to support partial payments, payment plans, and multiple captures against a single encounter without creating reconciliation errors.

Pro Tip: Set up automated batch closing at a consistent time each day. Manual batch management in busy practices leads to missed settlements and delayed funding, which creates cash flow gaps that compound over time.

What compliance requirements apply to credit card processing in healthcare?

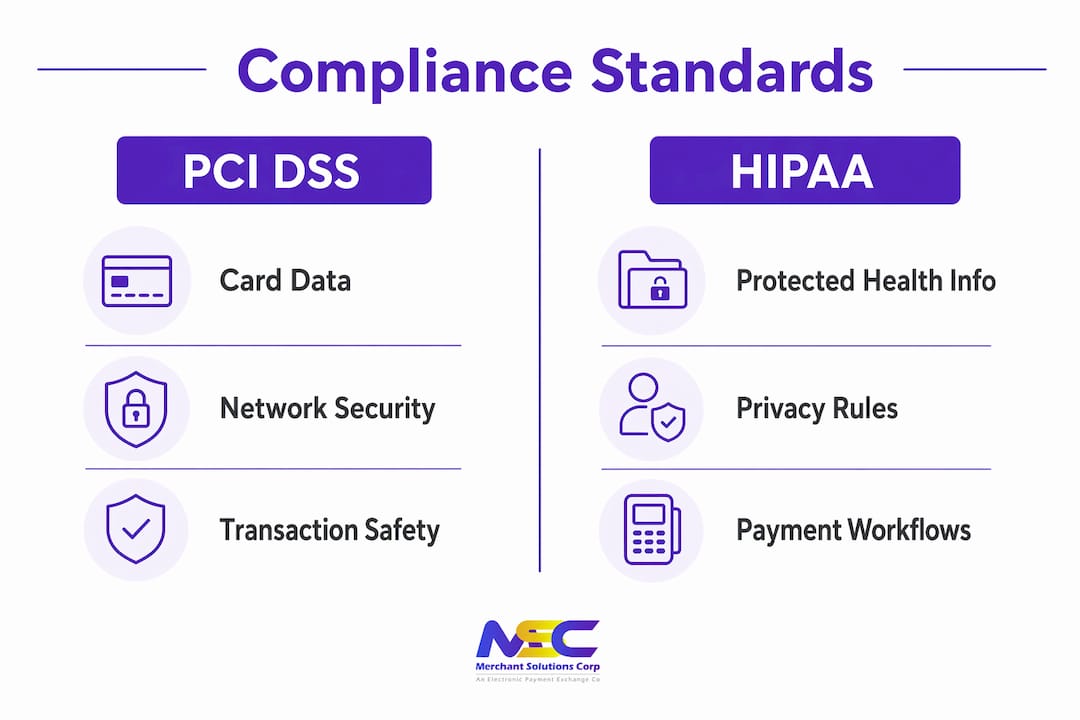

Compliance in healthcare payment processing is not a single checkbox. It requires layering two distinct security standards, each with different scope and enforcement mechanisms.

PCI DSS (Payment Card Industry Data Security Standard) applies to any organization that stores, processes, or transmits cardholder data. It covers card numbers, expiration dates, and CVV codes. Every healthcare provider accepting credit cards must meet PCI DSS requirements, regardless of size or specialty.

HIPAA applies when payment workflows create, receive, or transmit protected health information. HIPAA applies to payment workflows that involve ePHI, meaning a transaction that links a patient’s name, diagnosis, or account number to a payment record falls under HIPAA jurisdiction. Credit card numbers alone are a PCI matter. The moment a payment record includes a patient identifier alongside clinical or billing data, HIPAA governs that record too.

PCI compliance alone is not sufficient for HIPAA compliance when ePHI is involved in payment workflows. Organizations must layer both standards, which means your payment architecture, vendor contracts, and workflow design all need to satisfy both frameworks simultaneously.

When does a processor become a Business Associate?

A payment processor becomes a HIPAA Business Associate when it handles ePHI on your behalf. Many consumer processors will not sign a Business Associate Agreement (BAA), which disqualifies them from HIPAA-regulated healthcare payment workflows. If your processor touches any data that could identify a patient in connection with a health service, you need a signed BAA before processing a single transaction.

Common HIPAA pitfalls in payment processing:

- Emailing unencrypted receipts that include patient names, dates of service, or procedure codes

- Storing PHI in payment metadata, transaction notes, or analytics logs

- Using consumer-grade mobile payment apps that do not support BAAs

- Kiosk or self-service terminals that display or print PHI without access controls

- Call recordings from phone-based payment collection that capture diagnosis or treatment information

HIPAA violations in healthcare payments frequently stem from emailing unencrypted receipts or storing PHI in payment metadata and logs. Secure delivery and controlled access are not optional features. They are the baseline.

PHI also enters payment channels through non-obvious vectors. Call recordings, analytics logs, and payment descriptors can all inadvertently capture protected information, requiring vigilance in reducing PHI in card data capture paths and contractual safeguards with every vendor in your payment stack.

The critical distinction: HIPAA compliance is not guaranteed by a vendor claiming it. It requires the entire payment architecture, including contracts, workflow design, and hosting controls, to meet the standard. A processor that advertises “HIPAA-ready” without offering a BAA is not a compliant solution.

Practical safeguards include end-to-end encryption, tokenization of card data, role-based access controls, audit logs, and formal vendor agreements. Mapping your payment workflows to identify every point where ePHI could enter the transaction record is the most effective first step any practice can take.

How do HSA and FSA cards affect healthcare payment processing?

Health Savings Account (HSA) and Flexible Spending Account (FSA) cards function like prepaid debit cards restricted to qualified medical expenses. Accepting them correctly requires specific configuration at the terminal and processor level.

Merchant eligibility and MCC codes

Most healthcare providers are automatically eligible to accept HSA and FSA cards because their Merchant Category Code (MCC) identifies them as medical service providers. Pharmacies, hospitals, and physician offices typically fall into auto-approved MCC categories. However, businesses that sell a mix of eligible and non-eligible items, such as a pharmacy that also sells cosmetics or snacks, must obtain IIAS (Inventory Information Approval System) certification to separate eligible purchases at the point of sale.

HSA and FSA cards require merchant eligibility via MCC codes or IIAS certification, with split tender often necessary to handle partial balances. If a patient’s HSA card does not cover the full balance, your terminal must support split tender, meaning the patient can pay part with the HSA card and the remainder with a personal credit or debit card. Processors that do not support split tender will generate declines that frustrate patients and delay collections.

HSA vs. FSA: key processing differences

| Feature | HSA Card | FSA Card |

|---|---|---|

| Funding source | Patient-owned savings account | Employer-funded benefit account |

| Rollover | Unused funds roll over annually | Most funds expire at year-end |

| Spending deadline | No deadline | Annual deadline creates year-end surges |

| Eligibility verification | MCC-based or IIAS | MCC-based or IIAS |

| Split tender need | Common for partial balances | Common, especially late in benefit year |

Year-end FSA spending surges are a real operational consideration. Patients rush to use remaining FSA balances before the December 31 deadline, which creates transaction volume spikes in November and December. Your payment system should be tested for HSA and FSA acceptance well before that window. Testing real transaction scenarios before launch avoids declines and patient frustration that can damage the provider-patient relationship.

Enabling HSA and FSA acceptance also has a direct revenue impact. Patients who can pay with pre-tax dollars are more likely to pay at the time of service rather than waiting for a statement. That reduces days in accounts receivable and lowers the administrative cost of follow-up billing.

Which features should you prioritize when choosing a healthcare payment processor?

Selecting among the best credit card processors for healthcare requires evaluating more than processing rates. The right processor must fit your compliance obligations, your existing technology stack, and your patient payment experience goals.

Pricing models compared

Three pricing structures dominate the market. Interchange-plus pricing passes the actual card network cost through to you with a fixed markup, making it the most transparent model for high-volume practices. Flat-rate pricing charges a single percentage regardless of card type, which simplifies accounting but can cost more as volume grows. Tiered pricing groups transactions into qualified, mid-qualified, and non-qualified buckets, which often obscures true costs and tends to disadvantage healthcare providers whose patients frequently use rewards cards that fall into higher tiers.

Starting monthly fees in healthcare payment processors vary widely, from $0 for processors like Chase InstaMed and Square to $399 for platforms like Podium. That range reflects significant differences in feature sets, compliance support, and integration depth. A $0 monthly fee processor without EHR integration may cost more in staff time than a higher-fee processor that automates reconciliation.

Features that matter most for healthcare providers:

- EHR and PMS integration. Direct integration with systems like Epic, athenahealth, or Kareo eliminates manual data entry and reduces reconciliation errors. Providers evaluating EMR and EHR payment integration should confirm that the processor supports bidirectional data flow, not just one-way payment posting.

- BAA availability. Any processor handling ePHI must offer a signed BAA. Confirm this before signing any merchant agreement.

- Tokenization and encryption. Card data should never be stored in plain text. Tokenization replaces card numbers with non-sensitive tokens for recurring billing and payment plans.

- Multi-channel payment support. Patients expect to pay in the office, online, by text, and through a patient portal. Your processor should support all four without requiring separate merchant accounts.

- HSA and FSA acceptance. Confirm that your terminal and gateway are configured for HSA and FSA cards with split tender capability.

- Customer support hours. Healthcare offices operate on tight schedules. A processor with support only during standard business hours creates risk when a payment issue arises during a busy clinic day.

Healthcare payment processors offering full HIPAA compliance and strong EHR integration include Chase InstaMed and Square, with additional options from Stax, PaymentCloud, and Podium for various practice sizes and needs. Each serves different volume levels and specialties, so matching the processor to your specific practice profile matters more than choosing the most recognized name.

Pro Tip: Request a sample BAA from any processor you are evaluating before you discuss pricing. A processor that hesitates or cannot produce a BAA quickly is signaling that HIPAA compliance is not a core part of their product. Move on.

Virtual card payments also deserve consideration for provider-to-supplier transactions. Virtual cards improve operational speed and auditability compared to manual checks, with transaction-level controls that reduce fraud exposure. For practices managing supply chain payments alongside patient billing, virtual cards add a layer of financial control that paper checks cannot match.

Key takeaways

Effective credit card processing in healthcare requires layering PCI DSS and HIPAA compliance across every vendor, workflow, and technology in your payment stack.

| Point | Details |

|---|---|

| PCI and HIPAA both apply | PCI covers card data; HIPAA applies when payment records include patient identifiers or clinical data. |

| BAAs are non-negotiable | Any processor handling ePHI must sign a Business Associate Agreement before processing begins. |

| HSA and FSA require configuration | Terminals must support split tender and correct MCC codes to avoid patient-facing declines. |

| Pricing model affects long-term cost | Interchange-plus is most transparent for high-volume practices; flat-rate suits lower-volume clinics. |

| EHR integration reduces manual work | Bidirectional data flow between your processor and EHR eliminates reconciliation errors and staff time. |

What I’ve learned from watching healthcare payment setups go wrong

I have reviewed enough healthcare payment implementations to know that most problems are not technical. They are architectural. A practice will select a processor based on a low rate, sign up without requesting a BAA, and then discover six months later that their patient portal payments are flowing through a system that has no HIPAA coverage whatsoever. By that point, they have processed thousands of transactions through a non-compliant workflow.

The second most common mistake is treating HSA and FSA acceptance as a simple toggle. It is not. The eligibility logic, split tender configuration, and IIAS certification requirements create real friction if you do not test them in a live environment before going live with patients. I have seen practices launch new payment systems in October, right before the FSA year-end rush, without testing HSA card scenarios. The result is a flood of declines during the busiest payment period of the year.

What actually works is starting with workflow mapping. Before you evaluate a single processor, document every point in your revenue cycle where a patient’s name, account number, or clinical data touches a payment record. That map tells you exactly where PHI exposure exists and what compliance controls you need at each point. It also tells you which processors are actually qualified to handle your workflow versus which ones are simply marketing themselves as healthcare-friendly.

The long-term cost savings from getting this right are real. Practices that invest in transparent pricing, proper compliance architecture, and integrated payment tools spend less on manual reconciliation, fewer staff hours on billing disputes, and face lower risk of regulatory penalties. The upfront work pays for itself within the first year.

— Jonathan

How Merchantsolutionscorp supports healthcare payment processing

Merchantsolutionscorp offers payment processing solutions built for the specific demands of healthcare and clinic environments. The platform supports credit card and ACH processing, HSA and FSA card acceptance, and dual pricing options that help offset processing fees without passing friction to patients. POS systems including Clover and mobile terminals are available with $0 upfront hardware programs, making it straightforward to upgrade your payment infrastructure without capital expense. For practices evaluating medical clinic payment solutions, Merchantsolutionscorp provides dedicated onboarding support and configuration assistance from day one. Contact the team to discuss a setup tailored to your practice size and compliance requirements.

FAQ

What is the difference between PCI and HIPAA in payment processing?

PCI DSS governs the security of credit card data, while HIPAA governs protected health information. When a payment record links a patient identifier to a health service, both standards apply simultaneously.

Does every healthcare payment processor need to sign a BAA?

A processor must sign a Business Associate Agreement only when it handles ePHI on your behalf. If the processor never accesses patient identifiers or clinical data, a BAA may not be required, but most healthcare billing workflows do involve ePHI.

Can patients use HSA and FSA cards at any medical office?

Most medical providers are eligible to accept HSA and FSA cards based on their Merchant Category Code. Providers selling mixed eligible and non-eligible items need IIAS certification to separate qualifying purchases at checkout.

What pricing model is best for a medical practice?

Interchange-plus pricing is generally the most cost-effective model for practices with consistent transaction volume because it passes actual network costs through with a fixed markup, making fees predictable and auditable.

How do card-not-present transactions affect healthcare billing costs?

Card-not-present transactions, including online payments, phone collections, and patient portal billing, carry higher processing rates and greater fraud risk than in-office card-present transactions. Practices with high CNP volume should account for this in their cost modeling.