Why Contractors Need Secure Payments: 2026 Guide

Why Contractors Need Secure Payments: 2026 Guide

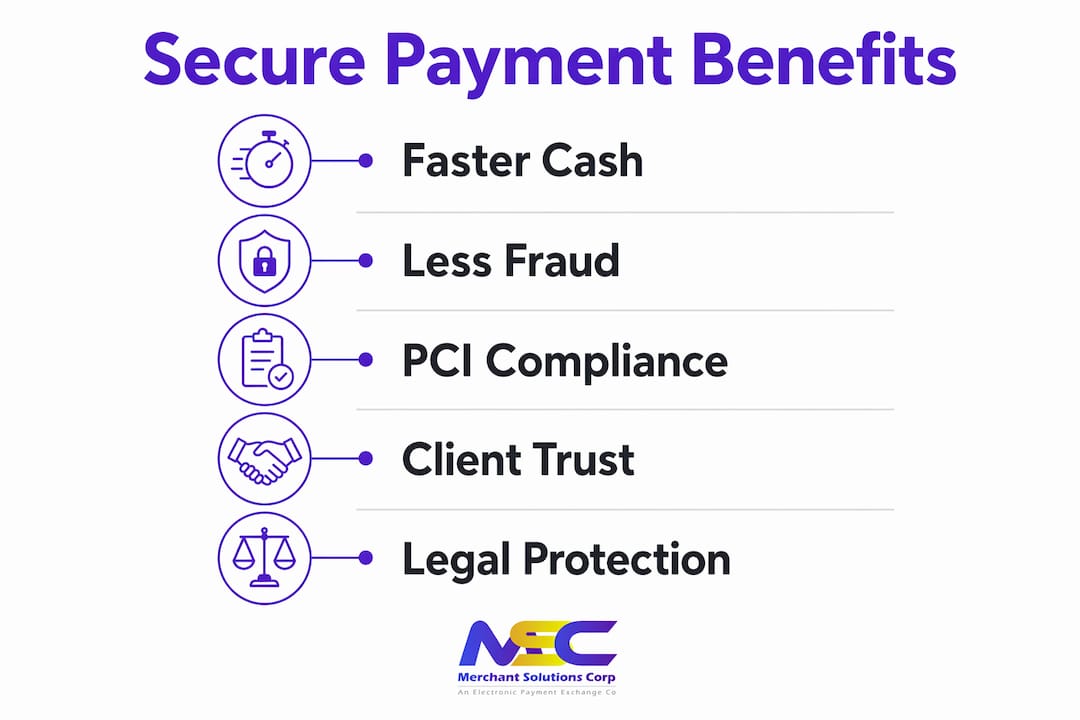

Secure payment systems for contractors are defined as digital payment infrastructure that protects financial transactions through encryption, tokenization, and compliance standards like PCI DSS. Contractors face real financial exposure when payment processes are weak. Fraud, delayed cash flow, and legal liability from mishandled card data can destabilize a contracting business faster than a bad project. Understanding why contractors need secure payments is the first step toward protecting your revenue and your reputation.

Why contractors need secure payments to protect cash flow

Payment delays are one of the most damaging problems in contracting. Traditional methods like paper invoices, personal checks, and bank wire transfers routinely take 30–60 days to clear. That gap forces contractors to cover labor and materials out of pocket while waiting for money they have already earned.

Modern secure payment systems close that gap dramatically. Digital payment links and virtual terminals bring collection times down to 1–2 business days. That shift changes everything about how you manage a job site budget.

Milestone invoicing is where secure digital payments prove their value most clearly. When you tie a payment link to a specific project stage, such as foundation completion or framing sign-off, clients pay against a defined deliverable. The payment arrives fast, and both parties have a clear record of what was paid and when.

Digital payment links also create timestamped audit trails that show exactly when a link was sent, when the client opened it, and when payment was made. That record is your best defense in a dispute. No more “I never received that invoice” conversations.

Key benefits of secure digital payments for cash flow:

- Payments collected in 1–2 business days instead of 30–60 days

- Milestone payments tied to project stages reduce funding gaps

- Timestamped records eliminate invoice disputes

- Clients can pay by text or email link from any device

- Faster deposits mean you can pay suppliers and crews on time

Pro Tip: Set up payment links for each project milestone before work begins. Send the link the moment a stage is complete. Clients pay faster when the process requires zero effort on their end.

What technologies actually make contractor payments secure?

PCI DSS compliance is the baseline standard for any contractor accepting card payments. PCI DSS stands for Payment Card Industry Data Security Standard. It sets the rules for how card data must be handled, stored, and transmitted. Violating those rules exposes you to fines, chargebacks, and potential loss of your ability to accept cards at all.

The most common PCI violation contractors commit happens on the phone. Manually entering a client’s card details during a phone call is a direct PCI compliance violation. It increases your legal liability and puts your client’s financial data at risk. The fix is straightforward: use Voice Checkout or a secure payment link so the client enters their own card details directly.

Here are the core technologies that protect contractor payment transactions:

-

Tokenization. Tokenization replaces a client’s actual card number with a unique digital token. That token is useless to a thief because it cannot be used outside your specific payment system. Contractors using tokenized payment methods see fraud reduced by about 30% and payment approval rates increase by 3–4%. Higher approval rates mean fewer failed transactions and fewer awkward follow-up calls.

-

End-to-end encryption. Encryption scrambles card data the moment a client enters it. The data travels from the client’s device to the payment processor in a form that cannot be read by anyone intercepting it. No readable card numbers ever pass through your system.

-

3-D Secure 2.3.1. This authentication protocol adds a verification step for high-risk transactions. 3-D Secure 2.3.1 challenges suspicious transactions only, so low-risk payments go through without friction. Clients experience a smooth checkout, and you get stronger fraud protection.

-

Real-time payment rails with fraud controls. Systems like FedNow and RTP process payments instantly while applying fraud screening in real time. This means you get paid fast without sacrificing security.

-

Multifactor authentication. Requiring a second verification step, such as a one-time code sent to a phone, protects your payment portal from unauthorized access. Even if a password is compromised, a thief cannot reach your funds.

“Secure payments use encryption, tokenization, multifactor authentication, and real-time rail controls to reduce fraud and false declines. 3-D Secure 2.3.1 improves security and user experience by challenging high-risk transactions only.” — KBV Research, Payment Security Guide

Understanding payment security compliance before you choose a payment platform saves you from costly mistakes later.

Credit cards, ACH, escrow, and cash: which is safest for contractors?

Not all payment methods carry the same level of protection. Credit cards, ACH transfers, escrow accounts, and cash differ widely in security, cost, speed, and dispute protection. Choosing the wrong method for a large project can leave you with no recourse if something goes wrong.

| Payment Method | Security Level | Speed | Cost | Best Use Case |

|---|---|---|---|---|

| Credit card | High | 1–2 business days | Moderate processing fee | Deposits, milestone payments, smaller jobs |

| ACH bank transfer | High | 1–3 business days | Low fee | Large commercial invoices |

| Escrow account | Very high | Varies by release terms | Setup fee may apply | Large projects with phased releases |

| Cash | Very low | Immediate | No fee | Not recommended for contracts |

ACH bank transfers carry lower processing fees than credit cards and work well for large commercial invoices. They integrate with secure payment platforms and provide a clear bank record of every transaction. For a $50,000 commercial job, the fee savings over credit card processing are significant.

Escrow accounts offer the strongest protection for both parties on large projects. Funds are held by a neutral third party and released only when defined milestones are met. This structure protects you from non-payment and protects the client from paying for work not yet completed.

Cash is the weakest option by every measure. Avoid cash and untraceable payment methods because they provide no dispute protection, no audit trail, and no recourse if a client claims they paid more or less than they did. A contractor who accepts cash for a $20,000 renovation has no documentation if the client disputes the amount later.

Secure, traceable payments linked to project milestones protect both you and your client. That protection builds trust and makes repeat business more likely.

How to implement secure payments in your contracting business

Adopting secure payment systems does not require a complete overhaul of how you run your business. A few targeted changes deliver most of the protection and speed improvements.

Steps to get started:

- Choose a platform with built-in PCI compliance. Never build your own payment flow. Use a platform that handles PCI DSS requirements automatically so you are never responsible for storing raw card data.

- Set up digital payment links for every invoice. Send payment links by text or email at each project milestone. Clients pay in minutes, and you get a timestamped record automatically.

- Enable tokenization on your account. Most modern payment platforms offer tokenization by default. Confirm it is active. The fraud reduction benefit of roughly 30% is too significant to leave on the table.

- Never type a client’s card number manually. If a client calls to pay by phone, send them a secure payment link instead. This keeps you PCI compliant and keeps their data safe.

- Activate 3-D Secure for card-not-present transactions. Any payment taken online or over the phone qualifies as card-not-present. 3-D Secure adds authentication without slowing down low-risk transactions.

- Use mobile payment terminals on-site. Clover and Square mobile terminals let clients tap or insert their card at the job site. This eliminates the need to handle card details at all.

- Review your payment audit trail weekly. Check for failed payments, chargebacks, or unusual activity. Early detection limits damage.

Pro Tip: Integrate your payment platform with your invoicing software. When a payment link is paid, the invoice closes automatically. You spend zero time on manual reconciliation and your books stay accurate.

Reviewing your payment processing options before committing to a platform helps you match the right tools to your project types and client base.

Protecting your clients’ data is also part of your professional responsibility. Retail cybersecurity practices apply directly to contractors who store client financial information, even temporarily. A data breach damages your reputation as much as a failed project.

Key Takeaways

Contractors who adopt secure, digital payment systems collect faster, reduce fraud, and protect their business from legal liability at every stage of a project.

| Point | Details |

|---|---|

| Faster cash flow | Secure digital payment links cut collection time from 30–60 days to 1–2 business days. |

| PCI compliance is non-negotiable | Manually entering card data by phone violates PCI DSS and exposes contractors to legal liability. |

| Tokenization reduces fraud | Tokenized payments lower fraud rates by about 30% and raise approval rates by 3–4%. |

| Cash carries the highest risk | Cash payments lack dispute protection and audit trails, making them unsuitable for contract work. |

| Audit trails prevent disputes | Timestamped payment records show exactly when invoices were sent, opened, and paid. |

Payment security is a business foundation, not a feature

Contractors often treat payment security as something to address later, after the business is established. That thinking gets expensive fast. The contractors I see struggle most with cash flow are not the ones with bad clients. They are the ones using payment systems that were never designed for contract work.

Paper invoices and check payments made sense before digital alternatives existed. They do not make sense now. A contractor running a $500,000 annual revenue operation on paper invoices and 45-day payment cycles is essentially giving clients an interest-free loan every month. That money belongs in your account, not theirs.

The PCI compliance issue is the one that surprises contractors most. Many have been typing client card numbers into a terminal during phone calls for years without realizing it is a violation. The liability exposure from a single data breach in that scenario can exceed the cost of switching to a proper system many times over. Voice Checkout and secure payment links exist precisely to close that gap.

The contractors who build the most resilient businesses treat payment infrastructure the same way they treat their tools. You would not use a broken saw on a job site. A payment system that exposes you to fraud, delays your cash, or violates compliance standards is just as dangerous. The good news is that modern platforms make the upgrade straightforward. The technology is accessible, the costs are manageable, and the protection is immediate.

— Jonathan

How Merchantsolutionscorp supports contractor payment security

Merchantsolutionscorp provides nationwide payment processing built for businesses that need speed, security, and compliance support from day one. Contractors can accept credit cards, ACH transfers, and mobile payments through POS systems including Clover and mobile terminals, with no upfront hardware costs through free equipment programs. Every account includes built-in PCI compliance support, tokenization, and dual pricing options to offset processing fees. Secure payment processing through Merchantsolutionscorp also includes payment link tools that let you collect milestone payments by text or email, with full audit trail documentation included.

FAQ

Why do contractors need secure payments?

Contractors need secure payments to protect against fraud, ensure faster cash collection, and maintain PCI DSS compliance. Insecure payment methods expose contractors to chargebacks, legal liability, and cash flow gaps that can disrupt operations.

How do digital payment links help contractors get paid faster?

Digital payment links reduce collection time from 30–60 days to 1–2 business days by letting clients pay instantly via text or email. They also create timestamped records that simplify dispute resolution.

What is PCI compliance and why does it matter for contractors?

PCI DSS compliance is the Payment Card Industry Data Security Standard, which governs how card data must be handled. Contractors who manually enter client card numbers during phone calls violate PCI DSS and face fines and legal liability.

Is ACH or credit card better for large contractor invoices?

ACH bank transfers carry lower processing fees than credit cards and are better suited for large commercial invoices. Both methods provide secure, traceable records, making either a stronger choice than cash or checks.

What is tokenization and how does it protect contractors?

Tokenization replaces a client’s card number with a unique digital token that cannot be used outside your payment system. Contractors using tokenization see fraud reduced by about 30% and payment approval rates increase by 3–4%.