Why HVAC Businesses Need Credit Card Processing

Why HVAC Businesses Need Credit Card Processing

If you run an HVAC business and you’re still relying on checks and cash to collect payment, you’re leaving money on the table every single day. Understanding why HVAC businesses need credit card processing goes beyond convenience. It directly affects how fast money hits your account, how many jobs close without payment disputes, and whether customers choose you over a competitor who takes cards. This guide covers the operational benefits, fee management strategies, compliance requirements, and practical steps to build a payment workflow that actually works for a field service business like yours.

Table of Contents

- Key takeaways

- Why HVAC businesses need credit card processing

- Benefits of accepting credit cards in HVAC services

- Managing processing fees for HVAC businesses

- PCI DSS compliance for HVAC businesses

- How to implement card processing in your HVAC operation

- My take on payment workflows and HVAC cash flow

- How Merchantsolutionscorp supports HVAC payment processing

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cards close billing cycles faster | On-site card processing eliminates invoice chasing and funds your account within one to two days. |

| Most customers prefer paying by card | Nearly half of HVAC customers expect card payment options, and younger customers especially won’t settle for less. |

| Fees are manageable with a smart mix | Use credit cards for smaller jobs and ACH for large payments to keep your blended processing cost reasonable. |

| PCI DSS compliance is non-negotiable | Every business accepting cards must meet PCI DSS standards or face fines, penalties, and potential account termination. |

| Integration multiplies the benefit | Connecting payment processing to your scheduling and invoicing software removes admin overhead and reduces billing errors. |

Why HVAC businesses need credit card processing

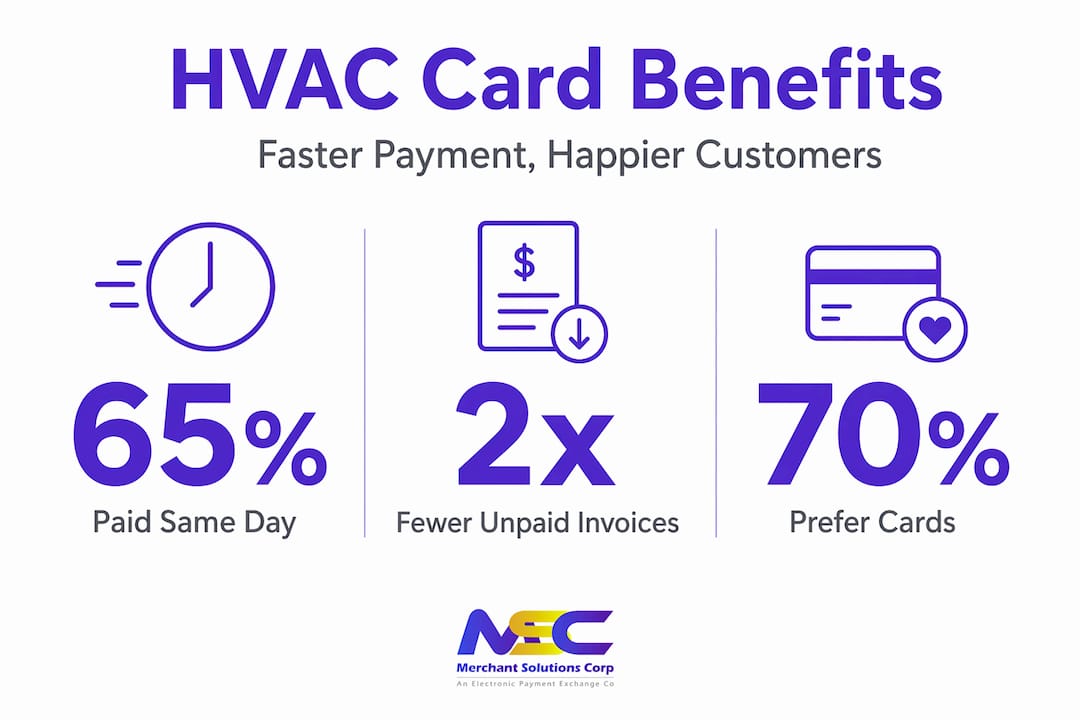

The typical HVAC service call ends one of two ways. The technician collects payment on the spot and moves to the next job, or the technician leaves an invoice and waits. That wait can stretch into days or weeks, and for a business running tight margins with equipment purchases, payroll, and fuel costs, that gap is painful.

The core problem with checks and cash in field service work is not just inconvenience. It’s structural. Checks introduce clearing delays of two to five business days, and bounced checks add bank fees and collection headaches on top. Cash is harder to track, easier to misplace, and requires additional handling to deposit. Neither method puts money in your account the same day the work is done.

Nearly half of HVAC service customers prefer paying by card over checks or cash, and customers under 40 especially expect digital payment options as a baseline, not a bonus. If you can’t meet that expectation, some of those customers will call someone who can.

Here’s what that looks like operationally:

- Accounts receivable aging increases. Every unpaid invoice over 30 days represents cash that isn’t available for your next supply order or payroll run.

- Collection costs rise. Chasing payments by phone and email takes staff time that could go toward scheduling, quoting, or customer follow-up.

- Job closure rates drop. When payment isn’t collected at the time of service, some customers delay, dispute, or disappear.

- Customer satisfaction suffers. A customer who wanted to pay by card and couldn’t will remember that friction the next time they need a tune-up or emergency repair.

The importance of payment options in HVAC is not theoretical. It has direct consequences on the speed of your cash flow and the quality of your customer relationships. Businesses that require cards already operate with a tighter billing cycle and lower outstanding receivables than those relying on invoices and paper checks.

Benefits of accepting credit cards in HVAC services

Moving to credit card acceptance changes the billing cycle in a way that most HVAC owners don’t fully appreciate until they experience it. On-site card processing closes the billing cycle immediately after job completion. Payment hits your account the same day or the next business day, with no invoice to send, no follow-up call to make, and no delay in your cash position.

Here are the core benefits, in order of operational impact:

-

Faster funding. Credit card payments typically settle in one to two business days. Compare that to waiting a week or more for a check to arrive, clear, and post. That difference compounds across dozens of jobs every month.

-

Payment certainty at the point of service. Accepting cards virtually guarantees payment at job completion. If a card declines, your technician knows immediately and can request an alternative on the spot. With a check, you often don’t know there’s a problem until days later.

-

Reduced billing disputes. When payment is processed at job completion with a digital receipt and itemized invoice, there’s a clear record. Customers who might dispute a mailed invoice rarely dispute a payment they approved and signed off on in person.

-

Better customer experience. Customers expect to pay with the method that’s most convenient for them. Offering cards signals that your business is professional, organized, and easy to work with.

-

Support for recurring payments and maintenance contracts. If you sell annual maintenance plans or service agreements, credit card processing lets you set up automatic billing. That creates predictable recurring revenue without any manual collection effort.

-

Less admin time on collections. Every hour your office staff spends chasing outstanding invoices is an hour not spent on scheduling, customer service, or growing the business. Integrated payment tools reduce disputes and AR aging, which directly reduces that administrative overhead.

The benefits of credit card processing for HVAC businesses are not limited to getting paid faster, though that alone justifies the change. The reduction in administrative burden, dispute risk, and collection effort creates operational gains that show up in your bottom line over time.

Pro Tip: Set up your field technicians with mobile card readers that connect to your invoicing software. When the technician collects payment on-site and the invoice closes automatically, you eliminate the gap between job completion and revenue recognition entirely.

Managing processing fees for HVAC businesses

The most common reason HVAC business owners hesitate on credit card processing is the cost. Processing fees are real, and they deserve an honest conversation rather than a vague reassurance that they’re worth it.

Credit card processing fees typically run around 3.5% of the transaction value. On a $200 service call, that’s $7. On an $8,000 system replacement, that’s $280. The math changes significantly depending on your job mix, and that’s exactly why fee management strategy matters.

| Payment method | Typical cost | Best use case |

|---|---|---|

| Credit card | 2.5% to 3.5% per transaction | Routine service calls, smaller repairs |

| ACH/bank transfer | Fixed fee, often $0.25 to $1.50 | Large system installs, commercial projects |

| Check | Minimal cost, plus risk of bounce | Large jobs where card fees are prohibitive |

The smartest approach for HVAC contractors is managing the payment method mix rather than trying to eliminate card fees entirely. Use credit cards as the default for quick convenience payments on routine calls. For large-ticket jobs like full system installs or commercial contracts, guide customers toward ACH or check to keep the effective blended cost down.

One real-world example illustrates this well. A contractor with $8 million in annual revenue who shifts a meaningful portion of large-job volume from cards to ACH can save roughly $84,000 per year in processing fees. That’s not a rounding error. That’s a meaningful margin improvement that funds equipment, staff, or growth.

When evaluating processors, ask about interchange-plus pricing rather than flat-rate pricing. Interchange-plus passes the actual card network cost to you with a fixed markup, which is typically more transparent and lower cost at volume. Flat-rate pricing is simpler but often more expensive when your transaction mix includes higher-value jobs.

Pro Tip: When quoting large jobs, mention both payment options early. Most customers are comfortable with ACH once they understand it’s secure and straightforward. Presenting it as a standard option rather than an afterthought increases uptake.

PCI DSS compliance for HVAC businesses

PCI DSS, which stands for Payment Card Industry Data Security Standard, is the security framework that governs how businesses handle cardholder data. PCI DSS is a mandatory contractual standard enforced through your acquiring bank and payment processor, not a government regulation. The practical outcome is the same, though. Fail to comply, and you face fines, penalties, and potential account termination.

This applies to your HVAC business whether you process cards in the field, through a terminal at your office, or through an online portal. Outsourcing your payment processing to a third-party provider reduces your compliance burden significantly, but it does not eliminate it. You are still responsible for how cardholder data is handled across your systems and by your staff.

Here are the practical compliance steps every HVAC business accepting cards should take:

- Complete your annual Self-Assessment Questionnaire (SAQ). The SAQ required for your business depends on how you process cards. Most field service businesses qualify for a shorter form.

- Use a PCI-compliant payment processor. Your processor should maintain their own certification and provide you with compliant hardware and software.

- Never store card data manually. Do not write down card numbers, store them in spreadsheets, or keep paper receipts with full card numbers visible.

- Train your technicians. Staff who handle card payments in the field need to understand basic security practices, including protecting the card reader from tampering.

- Review your network security. If you use a point-of-sale system connected to your business network, that network must meet baseline security requirements.

Working with a processor who actively supports your security compliance obligations simplifies this considerably. A good processor provides compliant hardware, handles data encryption and tokenization at the point of capture, and guides you through the SAQ process. Non-compliance risks include fines, account termination, and liability for any data breach that occurs. That risk is not worth accepting when compliant solutions are accessible and straightforward to implement.

How to implement card processing in your HVAC operation

Getting credit card processing in place is not complicated, but doing it well requires more than just plugging in a card reader. The goal is a payment workflow that closes jobs cleanly, syncs with your back-office systems, and requires minimal manual handling from your technicians.

Here’s how to build that workflow:

- Choose field-friendly hardware. Mobile card readers that connect via Bluetooth to a smartphone or tablet work well for technicians in the field. Look for devices that support chip, swipe, and NFC tap-to-pay, since customers use all three methods.

- Integrate with your scheduling and invoicing software. Integrated payment tools connect invoicing, scheduling, and accounting to remove double entry and reduce errors. When a technician collects payment, the invoice should close automatically in your system.

- Train your technicians on the payment process. A technician who is comfortable presenting the card reader and explaining payment options creates a better customer experience. Make it part of your standard job-close checklist.

- Set up recurring billing for maintenance contracts. If you offer annual service plans, configure automatic billing through your payment processor. This protects your recurring revenue without any manual follow-up.

- Offer multiple payment options strategically. Present cards as the default. Mention ACH as an option for larger jobs. Make both feel like natural choices rather than awkward requests.

- Monitor your payment metrics. Track days outstanding on invoices, dispute rates, and collection time weekly. These numbers tell you whether your payment workflow is actually performing or just running.

You can explore HVAC payment solutions in more depth to compare your options and identify the right mix for your specific job types and revenue volume. The right credit card solutions for HVAC businesses are the ones that fit your workflow, not the ones with the most features on a spec sheet.

My take on payment workflows and HVAC cash flow

In my experience working with field service businesses, the conversation about payment processing almost always starts in the wrong place. Business owners focus on the fee percentage. That’s understandable. But the fee is a known, fixed cost. The real variable is how much revenue you’re not capturing efficiently, and how much admin time you’re burning on collections.

What I’ve seen repeatedly is that HVAC businesses with tight payment workflows consistently outperform those with looser ones, regardless of which processor they use. On-site payment collection synchronized with invoicing software does something that a better processor rate simply cannot: it eliminates the gap between work completed and cash received. That gap is where disputes are born, where AR aging grows, and where cash flow pressure builds.

The other thing worth saying plainly is that accepting cards is now a baseline customer service expectation. It’s not a nice-to-have feature that signals a modern business. It’s a table-stakes requirement that a growing portion of your customer base will evaluate before they decide whether to book with you or someone else. Treating card acceptance as a reluctant concession to fees misses the point entirely.

The businesses I’ve seen get this right treat payment collection as part of the job, not an afterthought to it. They configure their systems so the technician collects payment at job close, the invoice syncs automatically, and the owner sees settled revenue by the next morning. That’s not complexity. That’s a well-built workflow.

— Jonathan

How Merchantsolutionscorp supports HVAC payment processing

If you’re ready to move beyond checks and invoices, Merchantsolutionscorp offers payment processing solutions built for businesses that work in the field and need reliable, fast payment collection. The platform supports credit card and ACH processing, mobile card readers, and POS systems that integrate with your existing invoicing and scheduling software.

Merchantsolutionscorp also offers dual pricing options that help offset processing fees, transparent pricing structures, and full PCI compliance support so you’re not navigating security requirements on your own. Hardware programs with no upfront cost make it easier to get set up without a large initial investment. Whether you run a single technician or a multi-crew operation, the platform scales with your volume and job mix. You can review processing pricing to understand your cost structure before you commit, so there are no surprises once you’re up and running.

FAQ

Why do HVAC businesses need credit card processing?

HVAC businesses need credit card processing to speed up cash flow, reduce unpaid invoices, and meet customer payment expectations. Nearly half of service customers prefer paying by card, and on-site card processing closes the billing cycle immediately after job completion.

What are the typical fees for HVAC credit card processing?

Credit card processing fees typically range from 2.5% to 3.5% per transaction. HVAC businesses can reduce their effective blended cost by routing large-ticket jobs through ACH or check while keeping cards as the default for routine service calls.

Is PCI DSS compliance required for HVAC businesses accepting cards?

Yes. PCI DSS compliance is a mandatory contractual requirement for any business that accepts credit cards, regardless of size or transaction volume. Non-compliance can result in fines, account termination, and liability for data breaches.

How can HVAC businesses accept payments in the field?

HVAC businesses can accept payments in the field using mobile card readers connected to a smartphone or tablet. These devices support chip, swipe, and NFC tap-to-pay methods and can integrate with scheduling and invoicing software to close jobs automatically at the point of payment.

Does accepting credit cards really improve cash flow for HVAC companies?

Yes. Credit card payments typically settle in one to two business days, compared to the week or more it can take for a check to arrive and clear. Combined with on-site collection at job completion, card processing significantly reduces accounts receivable aging and the admin time spent chasing outstanding invoices.