Why Lawyers Need Merchant Accounts: 2026 Guide

Why Lawyers Need Merchant Accounts: 2026 Guide

A merchant account is a specialized bank account that enables lawyers to accept credit card, debit card, and ACH payments from clients while maintaining the strict financial separation that legal ethics require. Understanding why lawyers need merchant accounts goes beyond simple payment convenience. It touches on professional responsibility, client trust fund protection, and the competitive reality that 40% of clients will not consider hiring a firm that lacks modern electronic payment options. For attorneys managing retainers, billing cycles, and IOLTA accounts, a general-purpose payment processor is not enough. The right merchant account is a compliance tool as much as a financial one.

Why lawyers need merchant accounts: the core case

Merchant accounts for attorneys are not the same product as the merchant accounts used by retail stores or restaurants. The legal profession operates under bar association rules that govern exactly how client funds must be held, tracked, and disbursed. A standard merchant account, such as those offered by Stripe or PayPal, treats every transaction as a simple deposit or withdrawal. That model creates serious ethical risk for law firms.

The core problem is fund separation. Lawyers must keep client funds in a dedicated trust account, often called an IOLTA (Interest on Lawyers’ Trust Accounts) account, completely separate from the firm’s operating funds. When a client pays a retainer, that money belongs to the client until the attorney earns it. A general payment processor has no mechanism to route funds correctly between trust and operating accounts. It also has no way to prevent processing fees from being deducted from client trust funds, which is an ethical violation in most states.

Legal-specific merchant accounts solve this by design. They route payments automatically to the correct account based on payment type, and they protect trust accounts from chargebacks by pulling disputed funds from the operating account rather than client funds. That single feature alone justifies the switch from a generic processor.

How do merchant accounts work differently for law firms?

The mechanics of a legal merchant account differ from a standard setup in three critical ways: fund routing, fee handling, and chargeback protection.

Fund routing is the foundation. Law firms typically need multiple merchant IDs to separate billing activities, deposits, and trust accounts. Each merchant ID connects to a specific bank account, so when a client pays a retainer, the funds flow directly into the trust account. When a client pays an invoice for earned fees, the funds flow into the operating account. This separation happens automatically, without manual intervention from your staff.

Fee handling is where generic processors create the most risk. Processing fees are typically deducted from the account that receives the payment. If a retainer payment lands in your trust account and the processor deducts its fee from that same account, you have just used client funds to pay a business expense. That is commingling, and it violates bar rules in virtually every jurisdiction. Legal-specific processors handle this correctly: processing fees are deducted only from the firm’s operating account, never from client trust funds.

Chargeback protection is the third differentiator. Chargebacks are a standard risk in payment processing. A client disputes a charge, and the processor reverses the funds while the dispute is investigated. For a retail business, that reversal comes from the operating account. For a law firm using a generic processor, that reversal could come directly from the trust account, reducing client funds without authorization. Legal merchant accounts prevent this by covering disputed amounts from operating funds instead.

- Automatic routing of payments to trust or operating accounts based on payment type

- Fee deductions taken only from the operating account, never from client funds

- Chargeback coverage funded from operating accounts to protect client trust balances

- Multiple merchant IDs to support distinct billing activities within one firm

- Detailed transaction records that simplify reconciliation and bar compliance audits

Pro Tip: When evaluating any payment processor, ask specifically whether they support IOLTA-compliant fund routing and whether their chargeback policy protects trust account balances. If a provider cannot answer both questions clearly, that is your answer.

What are the main benefits of merchant accounts for attorneys?

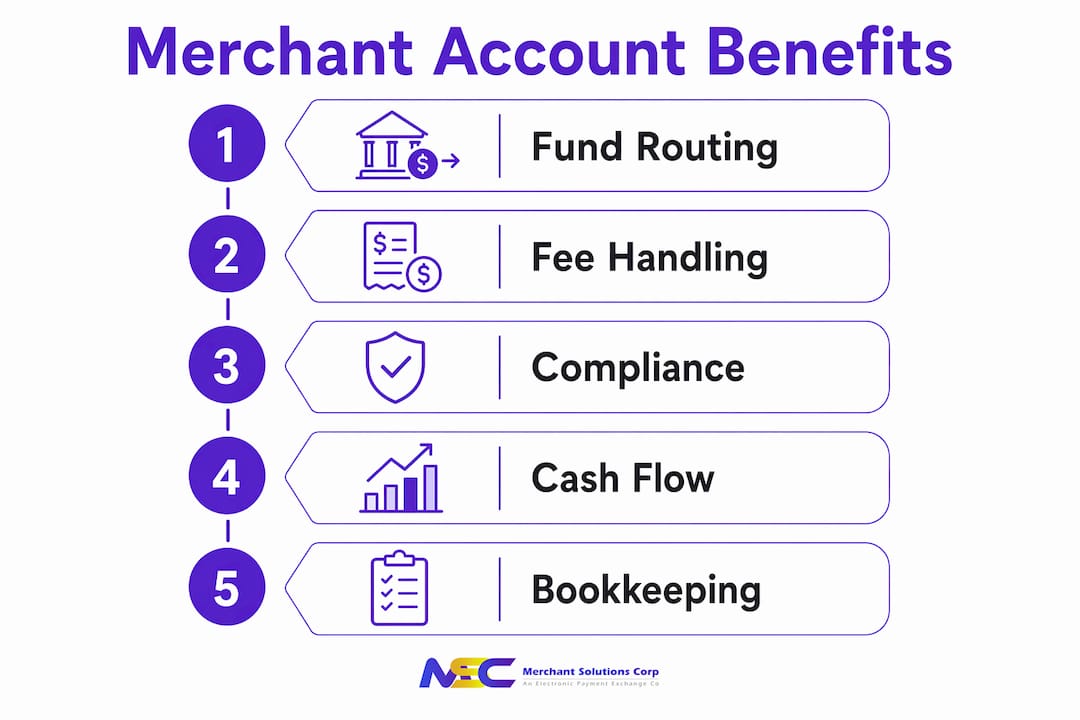

The benefits of merchant accounts for law firms extend well beyond compliance. They affect cash flow, client relationships, and the daily efficiency of your practice.

Faster, more reliable cash flow

Clients who pay by credit card or ACH pay faster than clients who mail checks. Merchant accounts create a regulated fund flow that supports recurring billing and produces more predictable revenue cycles. For firms that bill on retainer, the ability to set up automatic recurring payments means fewer collection calls and fewer gaps between billing periods.

A competitive edge that clients now expect

- Client acquisition: 78% of law firms now accept online payments, which means firms that do not are already in the minority. Clients notice.

- Hiring decisions: 50% of consumers are more likely to hire a lawyer who offers easy electronic payment options. That is not a preference. It is a deciding factor.

- Disqualifying factor: 40% of potential clients would not consider a firm that lacks modern payment methods. Every firm without a merchant account is invisible to a significant portion of the market.

- Client retention: Clients who can pay online, on their schedule, with a card they already use, report higher satisfaction. Convenience reduces friction at the most sensitive point in the client relationship: the billing conversation.

Simplified bookkeeping and reconciliation

Merchant accounts reduce manual bookkeeping work and help firms close their books faster with fewer errors. Payments are organized by account, matched to invoices automatically, and logged with timestamps and transaction IDs. For firms that face bar audits or trust account reviews, this level of documentation is not optional. It is protection.

Ethical compliance built into the process

The compliance benefit is the one most attorneys underestimate until they face a bar complaint. When your payment system automatically prevents commingling and protects client funds from chargebacks, compliance becomes a byproduct of your normal operations rather than a separate task requiring constant vigilance.

Generic vs. legal-specific merchant accounts: which one fits your firm?

Not all payment solutions for law firms are equal. The table below shows the key distinctions between standard merchant accounts and legal-specific merchant accounts.

| Feature | Standard merchant account | Legal-specific merchant account |

|---|---|---|

| IOLTA-compliant fund routing | No | Yes |

| Fee deduction from trust accounts | Yes (risk) | No (protected) |

| Chargeback protection for trust funds | No | Yes |

| Multiple merchant IDs for billing types | Rarely | Standard |

| Bar association compliance support | No | Yes |

| Trust account reconciliation tools | No | Yes |

| Designed for legal billing cycles | No | Yes |

Standard merchant accounts from general processors treat your law firm like a retail store. They see transactions as simple deposits and withdrawals with no mechanism to protect client funds held in trust or handle processing fees correctly. That design works for selling merchandise. It does not work for managing a client’s retainer.

Legal-specific processors are built around the ABA Model Rules and state bar requirements. They understand that a payment from a client is not always revenue. Sometimes it is a liability held in trust. The system must reflect that distinction at the transaction level, not just in your accounting software after the fact.

Pro Tip: Before signing any merchant account agreement, confirm that the provider has experience with law firms specifically. Ask for references from other attorneys, and verify that their fee agreement explicitly addresses trust account protection. A provider who is unfamiliar with IOLTA requirements is a liability, not an asset.

The risk of using a non-legal-specific account is not theoretical. Bar associations across the country have disciplined attorneys for commingling that resulted directly from using standard payment processors without understanding how fees and chargebacks are handled. The professional services payment solutions that work for law firms are those designed with these risks in mind from the start.

How to choose and implement a merchant account in your practice

Selecting the right merchant account is a decision that affects your ethics compliance, your client relationships, and your daily operations. Approach it with the same rigor you would apply to any major vendor relationship.

Criteria for selecting a legal-compliant provider

- IOLTA compliance: The provider must support automatic routing of funds to trust and operating accounts. This is non-negotiable.

- Fee protection: Confirm in writing that processing fees will never be deducted from trust account balances.

- Chargeback policy: Verify that disputed funds are covered from operating accounts, not client trust funds.

- Multiple merchant IDs: Your firm likely handles retainers, earned fees, and cost advances separately. The provider must support distinct merchant IDs for each.

- Integration with practice management software: Look for compatibility with platforms like Clio, MyCase, or PracticePanther to reduce manual data entry.

- PCI DSS compliance: The provider must meet Payment Card Industry Data Security Standards to protect client payment data.

- Transparent pricing: Understand whether the provider uses interchange-plus pricing or flat-rate pricing, and calculate the real cost for your transaction volume.

Steps for applying and integrating your merchant account

Applying for a merchant account involves submitting documentation similar to opening a business bank account. You will need your firm’s EIN, business registration documents, bank account information for both trust and operating accounts, and recent financial statements. The underwriting process reviews your firm’s financial history and transaction volume to assess risk.

Once approved, integration involves connecting the merchant account to your practice management software, configuring fund routing rules for each account type, and training staff on the payment workflow. Most legal-specific providers offer onboarding support to walk your team through the setup. The step-by-step payment processing guide from Merchantsolutionscorp covers the fundamentals that apply to professional service firms of any size.

Communicating payment options to clients

Clients should know your payment options before they receive their first invoice. Include accepted payment methods in your engagement letter. Add a payment portal link to your invoices. Display accepted card types on your website. When clients know they can pay by card, ACH, or online portal, the billing conversation becomes simpler and payment timelines shorten.

Merchant accounts allow acceptance of multiple payment types through a single account, which means you can offer clients credit cards, debit cards, and ACH transfers without managing separate systems. That flexibility matters to clients who prefer different payment methods for different transactions.

Key takeaways

A legal-specific merchant account is the only payment processing solution that protects client trust funds, prevents commingling, and keeps your firm compliant with bar association rules while meeting modern client payment expectations.

| Point | Details |

|---|---|

| Trust account protection | Legal merchant accounts route funds and cover chargebacks from operating accounts, never from client funds. |

| Compliance by design | Automatic fee deduction from operating accounts prevents the commingling violations that trigger bar complaints. |

| Competitive necessity | 40% of clients will not hire firms without modern payment options, making merchant accounts a business requirement. |

| Bookkeeping efficiency | Organized transaction records and automatic reconciliation reduce manual work and support bar audits. |

| Provider selection matters | Only legal-specific processors support IOLTA compliance, multiple merchant IDs, and trust account safeguards. |

The payment gap most law firms still haven’t closed

After years of working with professional service businesses, the pattern is clear: law firms are often the last professional services category to modernize their payment infrastructure, and they pay for that delay in ways that go beyond lost clients.

The compliance risk is the part that surprises attorneys most. Many lawyers assume that any payment processor will work as long as they manually track which funds belong to clients. That assumption is wrong. Manual tracking does not prevent a processor from deducting fees from a trust account. It does not stop a chargeback from pulling funds out of client balances. The system has to handle these protections automatically, because the moment a human step is required, the risk of error becomes a risk of a bar complaint.

The competitive reality is equally stark. Clients now expect the same convenience from their attorney that they get from their accountant, their doctor, and their online retailer. Failing to offer modern payment methods is a significant competitive disadvantage. Clients avoid firms that do not provide it. That is not an opinion. It is documented behavior.

The firms that get this right treat their merchant account setup as a one-time investment in both compliance and client experience. They choose a provider with legal expertise, configure the system correctly from day one, and then let the automation handle the compliance work. The firms that get it wrong spend years patching manual processes and hoping the bar never looks too closely.

The right merchant account does not just process payments. It protects your license.

— Jonathan

How Merchantsolutionscorp supports law firm payment processing

Merchantsolutionscorp works with professional service businesses across the US and Canada, including law firms that need payment systems built for compliance and efficiency. The platform supports credit card processing, ACH payments, and virtual terminals that let attorneys accept payments remotely and securely. With tailored payment processing solutions designed for professional services, Merchantsolutionscorp helps firms configure fund routing, manage transaction records, and reduce processing costs through dual pricing options. Whether your firm is setting up its first merchant account or replacing a generic processor that lacks legal compliance features, Merchantsolutionscorp provides the setup support and ongoing service your practice needs. Contact Merchantsolutionscorp to discuss a payment solution built for how law firms actually operate.

FAQ

What is a merchant account for lawyers?

A merchant account for lawyers is a specialized payment processing account that enables law firms to accept credit cards, debit cards, and ACH payments while automatically routing funds to the correct trust or operating account. Unlike standard merchant accounts, legal-specific accounts include IOLTA compliance features and trust account protections.

Do lawyers need a separate merchant account for trust funds?

Yes. Law firms typically need multiple merchant IDs to keep trust account payments separate from operating account payments. Using a single account for both creates commingling risk and potential bar violations.

Can lawyers use Stripe or PayPal for client payments?

Standard processors like Stripe and PayPal lack the mechanisms to protect client trust funds or handle processing fees correctly for legal billing. Using them for retainer payments creates a real risk of ethical violations related to commingling and improper fee deductions.

How do processing fees work with a legal merchant account?

With a legal-specific merchant account, processing fees are deducted only from the firm’s operating account, never from client trust funds. This fee protection is a core compliance feature that standard processors do not offer.

How long does it take to set up a merchant account for a law firm?

The application process involves submitting business registration documents, your EIN, bank account details, and financial statements for underwriting review. Most approvals take a few business days, with full integration into practice management software typically completed within one to two weeks.