Best Payment Processor for Canada Businesses in 2026

Best Payment Processor for Canada Businesses in 2026

Choosing the best payment processor for Canada businesses is one of the most consequential decisions you will make for your bottom line, yet most business owners make it based on the first advertised rate they see. That number rarely tells the whole story. Transaction fees, monthly minimums, PCI compliance charges, and add-on costs for invoicing or recurring billing can quietly double what you actually pay. This guide cuts through the noise, comparing the top payment processors Canada has to offer across pricing models, features, and operational fit, so you can make a decision grounded in real numbers and real business needs.

Table of Contents

- Key takeaways

- Understanding payment processing for Canadian businesses

- Top payment processors compared

- Operational factors beyond price

- How to choose the right processor for your business

- My perspective on what Canadian businesses get wrong

- How Merchantsolutionscorp supports Canadian businesses

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cheapest rate is rarely total cost | Hidden fees for PCI compliance, chargebacks, and add-ons often exceed the base transaction rate. |

| Pricing model matters more than rate | Interchange-plus pricing consistently outperforms flat-rate for higher-volume Canadian merchants. |

| PAD is underused and cost-effective | Pre-authorized Debit avoids card network fees entirely, making it ideal for recurring billing businesses. |

| Integration reduces operational cost | Processors that connect natively with your accounting or POS software save time and reduce bookkeeping errors. |

| Match processor to your business type | Retail, subscription, and e-commerce businesses have fundamentally different processing needs and cost profiles. |

Understanding payment processing for Canadian businesses

Before comparing providers, you need to understand what you are actually buying. Many business owners use the terms “payment processor” and “payment gateway” interchangeably. They are not the same thing, and confusing processor and gateway can lead to paying for redundant services or missing critical functionality.

Payment processor vs. payment gateway

A payment processor is the company that moves funds between your customer’s bank and yours. It handles authorization, settlement, and compliance. A payment gateway is the software layer that transmits transaction data securely between your website or terminal and the processor. Some platforms combine both functions. Others separate them, which gives you more flexibility but adds complexity.

Pricing models you will encounter

Understanding pricing models is non-negotiable before signing any merchant agreement. The three most common structures are:

- Flat-rate pricing: You pay a single percentage on every transaction regardless of card type. Simple to predict, but often more expensive for businesses processing high volumes or using corporate and rewards cards.

- Interchange-plus pricing: You pay the actual interchange rate set by card networks (Visa, Mastercard) plus a fixed processor markup. Interchange-plus typically benefits higher-volume merchants significantly compared to flat-rate structures.

- Tiered pricing: Transactions are bucketed into “qualified,” “mid-qualified,” and “non-qualified” tiers. This model is the least transparent and often the most costly. Avoid it if you can.

Pre-authorized Debit (PAD) explained

Pre-authorized Debit is a distinctly Canadian payments method that debits customer bank accounts directly, with the customer’s prior written or digital authorization. PAD avoids card network fees entirely, making it significantly cheaper than credit card processing for recurring charges such as subscriptions, rent collection, or membership fees.

Security and regulatory compliance

Any processor operating in Canada must comply with PCI DSS (Payment Card Industry Data Security Standard). Watch for processors that charge a separate monthly PCI compliance fee on top of transaction costs. Some bundle it; others charge $10 to $30 per month as a hidden line item. Canadian businesses also benefit from processors that support EMV chip, contactless NFC payments, and tokenization to protect cardholder data.

Pro Tip: Ask every processor you evaluate for a complete fee schedule in writing before signing. If they hesitate or obscure it, that tells you something important.

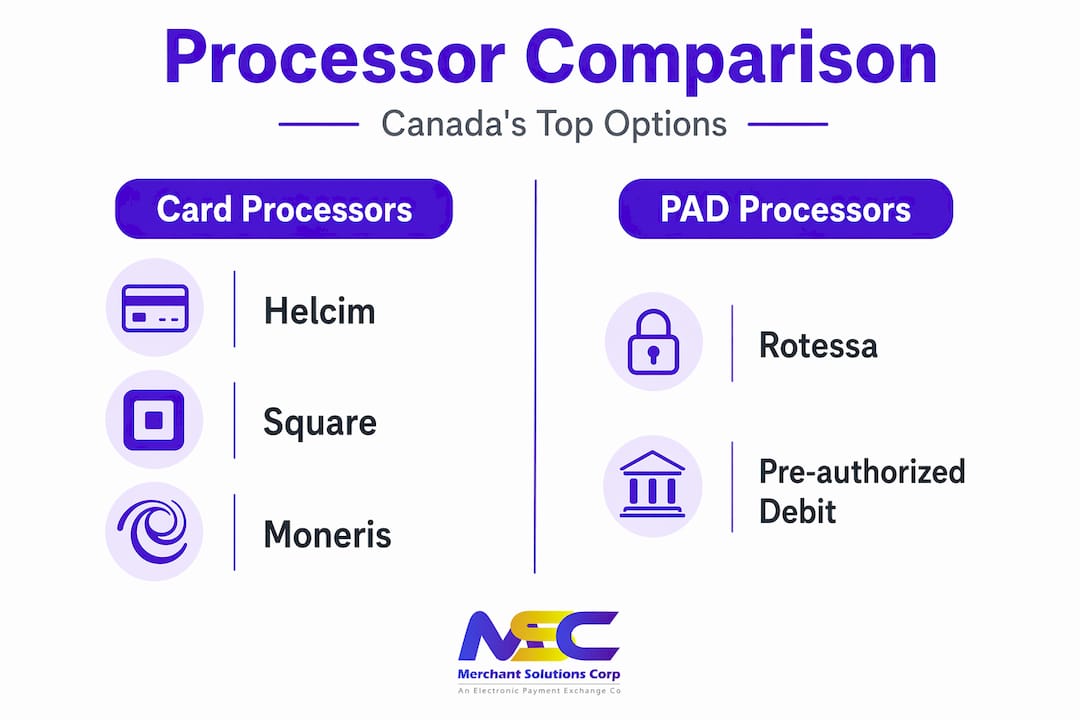

Top payment processors compared

The Canadian market has a handful of players that consistently appear when businesses go looking for the best payment gateway Canada can offer. Each serves a different business profile. Here is how they stack up.

Feature and pricing comparison

| Processor | Pricing model | Online transaction fee | Monthly fee | Best for |

|---|---|---|---|---|

| Helcim | Interchange-plus | Interchange + 0.40% + $0.08 | None | Growing businesses, high volume |

| Stripe | Flat-rate | 2.9% + $0.30 | None | SaaS, e-commerce, developers |

| Square | Flat-rate | 2.9% + $0.30 | None (paid tiers available) | Retail, food service, small businesses |

| Rotessa | Flat-fee PAD | Fixed tiers, no percentage fee | Tiered plans | Recurring billing, service businesses |

| Moneris | Tiered | Varies by plan | Monthly fee applies | Established retail, enterprise |

Helcim is a Canadian-founded processor built specifically for merchants who want pricing transparency. Its interchange-plus model charges interchange plus 0.40% and $0.08 per online transaction with no monthly fees and no separate PCI charges. For businesses processing more than $25,000 per month, the savings compared to flat-rate processors can reach 20 to 25 percent.

Stripe charges 2.9% plus $0.30 per transaction with custom rates available for merchants exceeding $250,000 annually. It is the preferred choice for software companies, online marketplaces, and businesses that need deep API customization for checkout flows.

Square works well for businesses that need both online and in-person payment capability without complex setup. It includes inventory management, invoicing, and basic reporting at no additional cost, which matters when you are calculating true total cost.

Rotessa focuses exclusively on PAD processing. It serves over 3,000 Canadian businesses with flat-fee, tier-based pricing that avoids percentage-based fees altogether. For a gym, property management company, or professional services firm collecting recurring payments, Rotessa can dramatically reduce processing costs compared to charging the same amounts to a credit card.

Moneris is the largest payment processor in Canada, jointly owned by RBC and BMO. It is reliable and widely supported for in-person retail, but its tiered pricing model and monthly fees make it less competitive for online or lower-volume businesses.

Pro Tip: If your business collects recurring payments from Canadian customers, get a PAD quote from a specialized provider like Rotessa alongside your credit card processing quotes. The cost difference on monthly billing cycles is often striking.

Other considerations worth noting:

- All-in-one platforms like Helcim and Square include invoicing, recurring billing, and inventory tools. Add-on creep from separate subscriptions to cover these features can quietly inflate your total cost by hundreds of dollars per year.

- For businesses with complex needs, decoupling your processor and gateway gives you the ability to support multiple payment rails and build custom checkout experiences.

Operational factors beyond price

Price gets you in the door, but it is the operational fit that determines whether a processor actually serves your business well over time. Several factors rarely appear in comparison articles but consistently affect the day-to-day experience of Canadian business owners.

Integration with your existing tools

A payment processor that does not connect to your accounting software, invoicing platform, or POS system creates manual work every time you reconcile. That manual work is a real cost, even if it does not appear on a fee schedule. Processors that sync automatically with accounting software improve bookkeeping accuracy and reduce the time your team spends matching transactions to invoices.

When evaluating Canada business payment solutions, ask specifically which accounting platforms the processor integrates with natively. QuickBooks, Xero, and Wave are the most common in the Canadian small business market. A native integration is always preferable to a third-party connector that adds another monthly fee and another potential point of failure.

Customer support quality

This is one of the most underrated factors in processor selection. Payment issues do not follow business hours. If a transaction fails during peak service or a chargeback arrives without explanation, you need someone you can reach quickly. Canadian businesses should ask whether support is available by phone, what the average response time is, and whether there is a dedicated account manager for your volume tier.

Fraud prevention and PCI compliance

Every processor you consider should support:

- Tokenization: Replaces card data with a unique identifier so sensitive information is never stored on your systems.

- 3D Secure authentication: Adds a verification step for online card-not-present transactions to reduce fraud liability.

- Custom fraud filters: Especially important for businesses with international customers, where rigid risk reduction settings can decline legitimate transactions and hurt revenue.

- Chargeback management tools: Some processors provide dispute management dashboards; others leave you to handle it manually.

Scalability for growing businesses

The processor that fits you today may not fit you in three years. If you are planning to expand into the US market, add new sales channels, or grow transaction volume significantly, choose a provider whose pricing scales favorably and whose technology can grow with you. Smarter payment routing and multi-currency support become relevant much earlier than most owners expect.

How to choose the right processor for your business

Knowing the options is one thing. Knowing which option fits your specific business is another. Here is a practical decision framework for Canadian business owners who want affordable payment processing without sacrificing functionality.

-

Calculate your monthly volume and average ticket size. If you process more than $20,000 per month, interchange-plus pricing will almost certainly save you money compared to flat-rate. Below that threshold, the simplicity of flat-rate may outweigh the marginal savings.

-

Identify your primary sales channel. Retail businesses with high in-person volume need strong POS integration and hardware options. E-commerce businesses need a payment gateway with reliable uptime, developer tools, and fraud filtering. Service businesses billing clients monthly should price out PAD as a primary or supplementary payment method.

-

List every feature you currently pay for separately. Invoicing software, recurring billing tools, inventory tracking, and reporting dashboards all carry costs. Processors that include these features natively can reduce your software stack and simplify operations, which has a measurable dollar value.

-

Evaluate PAD for recurring revenue. Service-based businesses that switch recurring charges from credit cards to PAD consistently improve their margins. PAD also reduces the risk of failed payments due to expired cards, which is a meaningful operational benefit for subscription or retainer-based businesses.

-

Request a full fee schedule before committing. Ask for the total cost of ownership: transaction fees, monthly fees, PCI compliance fees, chargeback fees, hardware costs, and any fees for features like recurring billing or batch payouts. Hidden fees layered on top of base transaction costs accumulate significantly over time and are the single most common source of surprise for business owners who chose a processor based on a headline rate.

-

Test customer support before you sign. Call the support line during business hours. Ask a technical question. Gauge how quickly and competently they respond. This interaction is a reliable indicator of how they will treat you when something actually goes wrong.

-

Think about where your business will be in two years. A processor that works well for a single-location retail store may not support a multi-location expansion, an e-commerce channel launch, or cross-border sales. Choose a platform you will not have to replace during a growth phase.

My perspective on what Canadian businesses get wrong

I have worked with enough Canadian businesses to notice a consistent pattern: owners spend a lot of time comparing headline transaction rates and almost no time calculating total cost of ownership. A processor charging 2.9% with no monthly fee sounds cheaper than one charging interchange-plus with a $15 monthly fee, but the math often does not support that assumption once volume climbs past $15,000 per month.

The second thing I see repeatedly is businesses running four or five separate software subscriptions because their processor does not include basic tools like invoicing or reporting. They are paying $30 a month for invoicing, $20 for reporting, and $15 for a recurring billing add-on, which completely erases any savings they got from choosing a “low-cost” processor.

What actually works is choosing a platform that handles the full transaction cycle. Not just the fee, but the invoice, the reconciliation, the reporting, and the customer communication. When you stop treating payment processing as a commodity and start treating it as an integrated operational system, the right choice becomes clearer.

I am also watching the growth of PAD closely. Service-based businesses, property managers, and subscription companies in Canada that have not yet explored PAD are leaving real money on the table. PAD adoption is growing precisely because business owners are doing that math and realizing the savings are substantial. The businesses that move early on this gain a structural cost advantage their competitors will struggle to match later.

My recommendation: start with a full cost audit of what you currently pay, then build your comparison from there. The right processor is the one that costs the least when every fee is counted and causes the least friction when something goes wrong.

— Jonathan

How Merchantsolutionscorp supports Canadian businesses

If you are working through this decision and want a solution that fits Canadian business operations without complexity, Merchantsolutionscorp is built for exactly that. The platform offers transparent payment processing pricing with no hidden add-on fees, covering credit card processing, ACH, and dual pricing programs that can offset transaction costs entirely.

Merchantsolutionscorp’s Canadian payment processing solutions include POS hardware options with $0 upfront through the free hardware program, making it accessible for businesses at any stage. Whether you run a retail location, a restaurant, or a service business with recurring billing needs, the platform scales with you. Setup is fast, support is available through onboarding and daily operations, and the systems integrate with the tools you are already using. Explore your POS system options or get started with a full payment processing overview to see which configuration fits your business.

FAQ

What is the best payment processor for small businesses in Canada?

Helcim and Square are consistently strong options for Canadian small businesses. Helcim suits higher-volume merchants with its interchange-plus pricing, while Square works well for lower-volume retail and food service businesses that need simple setup and included tools.

How does PAD compare to credit card processing in Canada?

Pre-authorized Debit is typically cheaper than credit card processing for recurring payments because it bypasses card network fees entirely. Providers like Rotessa offer fixed-tier pricing with no percentage-based fees, making PAD the more cost-effective option for service businesses billing clients regularly.

What hidden fees should Canadian businesses watch for?

Common hidden fees include PCI compliance charges ($10 to $30 per month), chargeback fees, batch settlement fees, and add-on costs for invoicing or recurring billing. Always request a complete written fee schedule before signing a merchant agreement.

Is interchange-plus pricing always better than flat-rate?

Interchange-plus pricing becomes more advantageous as your monthly processing volume increases. For businesses processing less than $10,000 to $15,000 per month, the simplicity and predictability of flat-rate pricing may outweigh the potential savings. Above that threshold, interchange-plus nearly always wins on total cost.

How do I choose between an integrated and a separate processor and gateway?

Integrated platforms like Square or Helcim are faster to set up and easier to manage, making them the right choice for most Canadian businesses. Separating your processor and gateway gives you more flexibility to build custom checkout flows and support multiple payment methods, but it adds technical complexity and is generally better suited to larger or developer-driven organizations.