Credit Card Fees Definition: A Guide for Business Owners

Credit Card Fees Definition: A Guide for Business Owners

![]()

Credit card fees are defined as the charges businesses pay to accept credit card payments, covering interchange fees, assessment fees, and payment processor fees. These costs typically range from 1.5% to 3.5% of each transaction’s value. On a $100 sale, that means $1.50 to $3.50 leaves your revenue before you see it. For business owners managing tight margins, understanding the credit card fees definition is not optional. It is the foundation of controlling your payment processing costs.

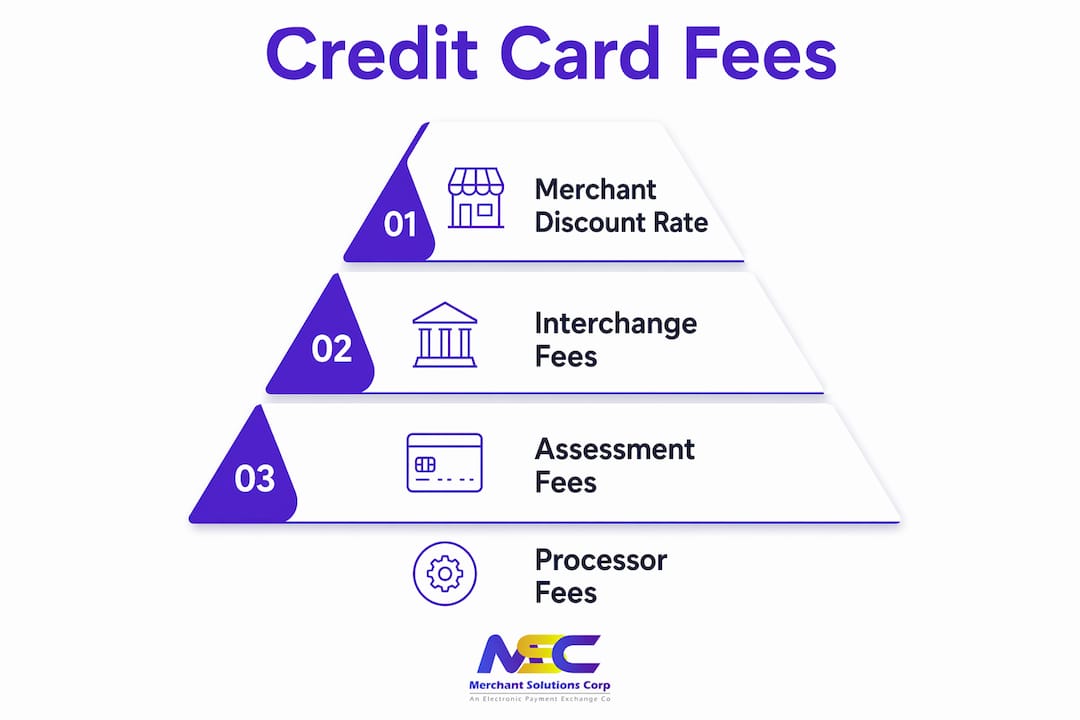

The three core components work together as the Merchant Discount Rate (MDR). Interchange fees go to the card-issuing bank. Assessment fees go to the card network, such as Visa, Mastercard, Discover, or American Express. Processor fees go to your payment processor. Each component behaves differently, and only one of them is negotiable. Knowing which one puts you in a stronger position at the table.

What are the main types of credit card fees businesses face?

Credit card fees consist of three distinct layers, and confusing them leads to poor decisions. Each layer has a different owner, a different rate, and a different level of flexibility.

Interchange fees

Interchange fees are paid to the bank that issued the customer’s credit card. They represent the largest portion of what you pay per transaction. Rates vary based on card type, transaction method, and industry category. A basic consumer Visa card carries a lower interchange rate than a premium travel rewards card. The card networks, not your processor, set these rates. That means interchange fees are non-negotiable for merchants.

Assessment fees

Assessment fees go directly to the card networks: Visa, Mastercard, Discover, and American Express. These fees are smaller than interchange but equally fixed. Visa and Mastercard publish their assessment schedules publicly. American Express historically charged higher rates because it acts as both the network and the issuer in many cases. Like interchange, you cannot negotiate assessment fees with your processor.

Payment processor fees

Processor fees are the markup your payment processing company charges on top of interchange and assessment. This is the only layer where negotiation is possible. The split between interchange and assessment fees on one side and processor fees on the other is the most critical distinction in fee management. Processors may charge a flat markup, a percentage, a per-transaction fee, or a combination of all three.

Understanding credit card fees also means recognizing how card type changes your cost. Rewards cards, corporate cards, and premium travel cards all carry higher interchange rates. The customer benefits from the rewards program, but you absorb the cost.

- Interchange fees: Paid to the issuing bank. Non-negotiable. The largest fee component.

- Assessment fees: Paid to card networks (Visa, Mastercard, Discover, AmEx). Non-negotiable. Smaller but fixed.

- Processor fees: Paid to your payment processor. Negotiable. The only lever you control.

- Merchant Discount Rate (MDR): The total of all three components expressed as a single rate.

- Card type surcharges: Rewards and premium cards trigger higher interchange rates automatically.

Pro Tip: When reviewing a processor contract, isolate the processor markup from the interchange and assessment pass-throughs. If a processor bundles everything into one opaque rate, ask for an itemized breakdown before signing.

How do pricing models affect credit card fees and costs?

The pricing model your processor uses determines how you experience these fees day to day. Three models dominate the market: flat-rate, interchange-plus, and tiered pricing. Each one distributes costs differently, and the right choice depends on your transaction volume and average ticket size.

-

Flat-rate pricing. Flat-rate pricing bundles interchange, assessment, and markup into a single predictable rate, such as 2.6% plus $0.10 per transaction. You pay the same percentage regardless of card type or transaction method. This model is popular with small businesses because it is easy to budget. The tradeoff is that you overpay on low-cost transactions and cannot benefit when a customer uses a basic debit card with a low interchange rate.

-

Interchange-plus pricing. Interchange-plus pricing separates interchange fees and adds a fixed processor markup on top. For example, you might pay interchange plus 0.3% plus $0.10 per transaction. This model is transparent. You see exactly what the network charges and exactly what your processor charges. High-volume businesses save money with this model because the processor markup stays fixed while the base interchange rate reflects the actual card used.

-

Tiered pricing. Tiered pricing groups transactions into qualified, mid-qualified, and non-qualified buckets. Each bucket carries a different rate. Processors decide which transactions fall into which tier, which creates limited transparency. A rewards card transaction might be pushed into the non-qualified tier, triggering the highest rate. This model benefits the processor more than the merchant.

-

Subscription or membership pricing. Some processors charge a flat monthly fee and pass interchange and assessment at cost with a small per-transaction fee. This model works well for businesses with high transaction volumes and consistent monthly activity.

-

Dual pricing. Dual pricing, also called cash discounting, displays two prices at checkout: one for cash and one for card payments. The card price includes the processing fee. This model shifts the cost to the customer who chooses to pay by card. It is legal in most US states when implemented correctly.

Flat-rate pricing is easier to budget but may cost more at high volume. Interchange-plus pricing offers savings for high-volume merchants because of its transparency and negotiability.

Pro Tip: Ask your processor for a 90-day transaction history analysis before switching pricing models. The data will show whether interchange-plus or flat-rate pricing saves you more based on your actual card mix and transaction methods.

What factors influence credit card fee rates and how can businesses manage them?

Merchant credit card fees are dynamic. Transaction method, card type, and pricing model can all shift your effective rate significantly. Business owners who treat processing fees as a fixed cost miss real savings opportunities.

The single biggest variable is whether the card is physically present at the time of sale. Card-present transactions, where the customer taps, swipes, or inserts their card, carry lower fees. Card-not-present transactions, such as phone orders or online payments, may add a 0.5% to 1.0% surcharge on top of the base rate. That difference adds up quickly for businesses with significant phone or online order volume.

The table below shows how transaction type and card type interact to affect your processing cost.

| Transaction type | Card type | Approximate fee range |

|---|---|---|

| Card-present (tap/chip) | Basic consumer debit | 1.5%–2.0% |

| Card-present (tap/chip) | Standard consumer credit | 1.8%–2.3% |

| Card-present (tap/chip) | Rewards or premium credit | 2.2%–2.8% |

| Card-not-present (online) | Standard consumer credit | 2.3%–3.0% |

| Card-not-present (online) | Rewards or premium credit | 2.8%–3.5% |

| Keyed-in (manual entry) | Any card type | 2.5%–3.5%+ |

Using payment terminals for keyed-in transactions triggers higher fees compared to swiping or tapping. Keyed-in entries also carry higher fraud risk, which is part of why networks charge more for them.

Practical steps to manage your processing costs include:

- Use EMV chip readers and NFC terminals. Card-present transactions with chip or tap technology qualify for lower interchange rates and reduce chargeback exposure.

- Encourage lower-cost payment methods. ACH transfers and debit cards carry lower fees than premium credit cards. A simple sign at the register can shift customer behavior.

- Negotiate your processor markup. Your transaction volume gives you leverage. Higher monthly volume means more bargaining power on the processor fee layer.

- Review your statements monthly. Fee creep is real. Processors sometimes add new line items or adjust markups between contract renewals.

- Avoid manual key entry when possible. Every keyed-in transaction costs more than a tapped or swiped one. A reliable terminal prevents this.

For businesses accepting payments through retail payment solutions, the terminal type and setup directly affect which fee tier applies to every transaction.

What are common consumer credit card fees and how do they differ from merchant fees?

Consumer credit card fees and merchant processing fees are entirely separate categories. Business owners sometimes conflate the two, which leads to confusion when analyzing costs. You do not pay your customers’ annual fees or late charges. Those belong to the cardholder’s relationship with their issuing bank.

Common consumer credit card fees include the following:

- Annual fees: Average approximately $28.25 per year for cards that charge them. Premium travel and rewards cards often charge $95 to $695 annually.

- Late payment fees: Average approximately $33.85, with initial fees potentially reaching $41 and repeat late fees climbing higher.

- Balance transfer fees: Typically 3%–5% of the transferred amount.

- Foreign transaction fees: Average approximately 1.58% of the transaction value.

- Interest charges (APR): Interest rates average around 22% APR for consumer credit cards carrying a balance.

These fees are charged by the issuing bank to the cardholder. They appear on the customer’s monthly statement, not on your merchant processing statement. Most consumer credit card fees can be avoided with responsible account management, including paying balances in full each month.

The practical implication for you as a business owner is clear. Your cost management focus belongs entirely on the merchant side: interchange rates, assessment fees, processor markup, and pricing model. Consumer fees are outside your control and outside your cost structure. Mixing up the two categories wastes time and energy that should go toward negotiating your actual processing costs.

Understanding this distinction also helps when customers ask why you charge a card surcharge or offer a cash discount. You can explain that your costs come from the card networks and banks, not from the customer’s personal card fees.

Key takeaways

Credit card fees are made up of three layers: interchange, assessment, and processor fees. Only the processor fee is negotiable, and your pricing model determines how much you pay across all three.

| Point | Details |

|---|---|

| Fee components | Interchange, assessment, and processor fees combine to form the Merchant Discount Rate. |

| Negotiability | Only processor fees are negotiable; interchange and assessment rates are set by card networks. |

| Pricing model impact | Interchange-plus pricing saves high-volume merchants more than flat-rate pricing. |

| Transaction method matters | Card-present transactions cost 0.5%–1.0% less than card-not-present transactions. |

| Consumer vs. merchant fees | Consumer fees like annual fees and late charges are separate from merchant processing costs. |

The fee structure most business owners get wrong

Most business owners I work with treat processing fees as a single, fixed line item. That framing costs them money every month. The reality is that your effective rate is a moving target shaped by card mix, transaction method, and the pricing model your processor sold you.

The most common mistake is accepting flat-rate pricing without questioning it. Flat-rate pricing is not inherently bad. For a low-volume business running under $10,000 per month in card sales, the simplicity is worth the slight premium. But for a restaurant or retail store processing $100,000 or more per month, that same flat rate becomes a significant overpayment compared to interchange-plus.

The second mistake is ignoring card-not-present fees. A business that takes phone orders without a proper virtual terminal setup ends up keying in transactions manually. That single habit can add a full percentage point to the effective rate on those sales. Switching to a payment processing setup with a proper virtual terminal or payment link fixes this immediately.

The third mistake is conflating consumer fees with merchant fees. When a customer mentions their card’s annual fee, that has no bearing on what you pay to accept it. What matters to you is whether that card is a basic consumer card or a premium rewards card, because the interchange rate differs significantly between the two.

Fee management is not a one-time task. Your card mix changes as your customer base evolves. Your transaction volume changes seasonally. Reviewing your processing statement every 90 days and benchmarking your effective rate against your pricing model keeps you ahead of unnecessary costs.

— Jonathan

How Merchantsolutionscorp supports better payment processing costs

Merchantsolutionscorp works with restaurants, retail businesses, and service companies across the US and Canada to lower the cost of accepting card payments. The platform offers payment processing pricing structures including interchange-plus and dual pricing options, so you pay based on your actual transaction mix rather than a bundled rate that benefits the processor. Hardware programs with $0 upfront costs mean you can upgrade to EMV chip and NFC terminals without capital outlay, which directly reduces your card-present transaction fees. The team supports businesses from onboarding through daily operations, including fee reviews and processor negotiations. For business owners ready to take a closer look at what they are actually paying, Merchantsolutionscorp provides the tools and support to make that analysis straightforward.

FAQ

What is the credit card fees definition for merchants?

Credit card fees for merchants are the charges paid to accept card payments, covering interchange fees to the issuing bank, assessment fees to the card network, and processor fees to the payment processor. These fees typically range from 1.5% to 3.5% per transaction.

Why are credit card fees charged to businesses?

Card networks and issuing banks charge fees to cover the cost of payment infrastructure, fraud protection, and cardholder rewards programs. Processors add their own markup for transaction routing, support, and technology services.

How can businesses reduce credit card fees?

Businesses reduce fees by switching to interchange-plus pricing, using EMV chip and NFC terminals for card-present transactions, and negotiating the processor markup directly. Encouraging lower-cost payment methods like ACH or debit also lowers the effective rate.

What is the difference between interchange fees and processor fees?

Interchange fees are set by card networks and paid to issuing banks. They are non-negotiable. Processor fees are the markup charged by your payment processor and are the only component open to negotiation.

Do merchants pay consumer credit card fees like annual fees or late charges?

No. Annual fees, late payment fees, and interest charges are paid by the cardholder to their issuing bank. Merchants pay only merchant-side processing fees based on transaction volume, card type, and pricing model.

Recommended

- Benefits of Zero Fee Payment Processing for Small Businesses | Merchant Solutions Corp

- Why HVAC Businesses Need Credit Card Processing | Merchant Solutions Corp

- Credit card processing for attorneys: boost revenue & get paid faster | Merchant Solutions Corp

- Set up payment processing: a simple guide for small businesses | Merchant Solutions Corp